Introduction

Two data points from late 2025 frame the question this piece tries to answer. First, spot HYPE ETFs debuted in the U.S. with reported first-day volume approaching $900M, extending the pattern established by spot BTC and ETH products: every new listed crypto wrapper draws institutional flow within hours. Second, a senior executive at hardware wallet maker Trezor publicly argued that the ETF format is the “worst outcome” for bitcoin — an accessibility win that hollows out the properties that made the asset worth accessing.

Both statements can be true. The ETF wrapper is the most successful distribution mechanism crypto has ever attached to itself; it is also a structural transformation of what holders own. Between the marketing gloss on one side and the ideological rejection on the other sits a set of plumbing questions that most coverage skips: who actually holds the coins, how do shares stay tethered to spot price, what happens during a stress event, and which of bitcoin’s original properties survive the wrapping.

This article walks through that plumbing. We look at the four-party architecture connecting sponsor, authorized participant, custodian, and market maker; the concentration of key custody in a single U.S. venue; the arbitrage mechanism that keeps net asset value tight; and the tradeoffs — legal, operational, and philosophical — that any holder of ETF shares implicitly accepts. The HYPE launch and the Trezor critique serve as contemporary anchors, but the structural questions apply equally to any spot crypto ETF now trading or waiting for approval.

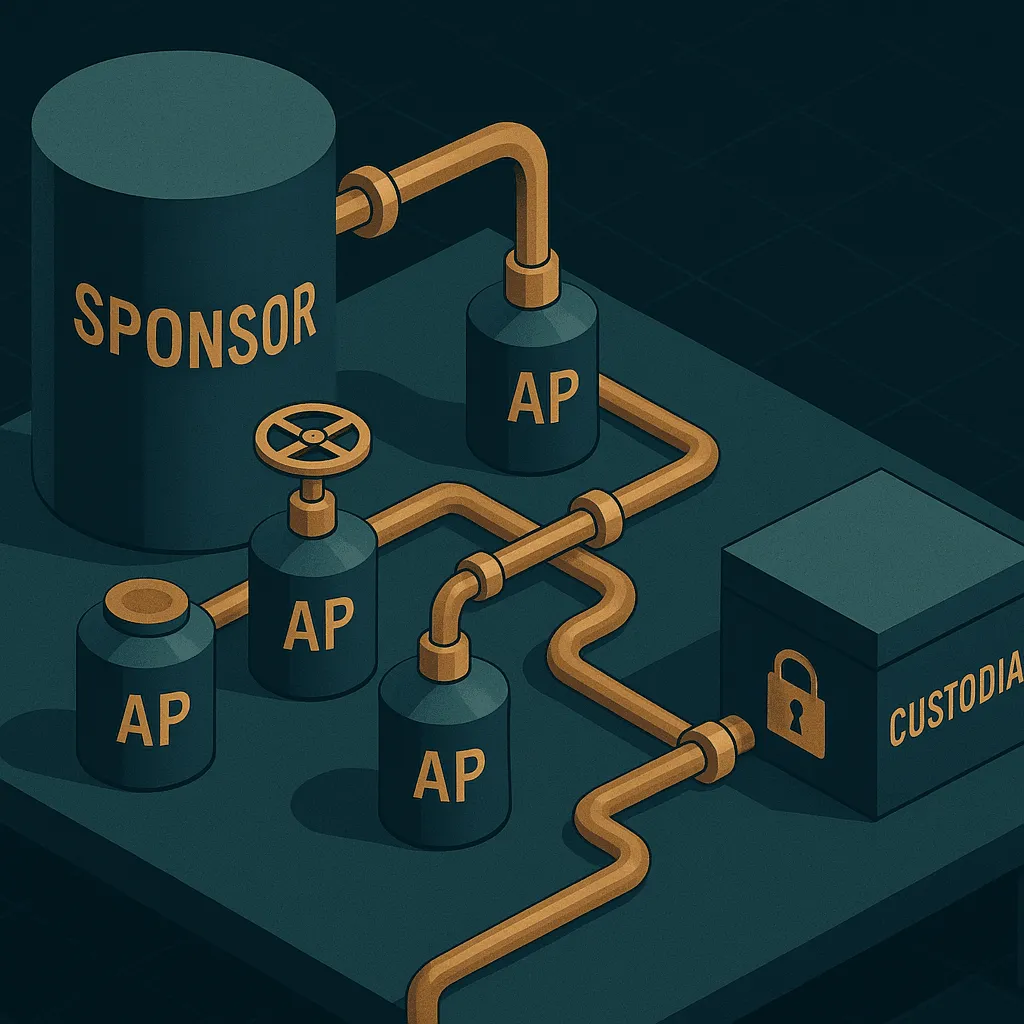

The four parties inside every spot crypto ETF

A spot crypto ETF is often described as if it were a passive container: coins go in, shares come out, price tracks. The reality is a coordinated dance between four distinct legal entities, each with its own incentives and its own points of failure.

The sponsor

The sponsor — BlackRock for IBIT, Fidelity for FBTC, Bitwise for its BITB product, and so on — is the fund’s issuer and marketer. The sponsor writes the prospectus, sets the expense ratio, hires the custodian, and takes management fees off the top of assets. The sponsor does not, however, hold the coins itself. It is closer to a general contractor than a warehouseman.

The sponsor’s core asset is a distribution relationship: brokerage platform integrations, financial advisor coverage, index inclusion, and the regulatory blessing to list on a national exchange. Those distribution rails are what a self-custodied bitcoin cannot access, and they are the entire commercial reason ETFs exist.

The authorized participant

The authorized participant (AP) is the mechanical heart of the structure. APs are typically large broker-dealers — Jane Street, Virtu, Cantor Fitzgerald, JPMorgan’s securities arm, and a handful of others in the U.S. market — that hold contractual rights to create and redeem shares directly with the fund.

When end-investor demand pushes ETF shares to a premium over NAV, an AP delivers the required basket (in current U.S. spot BTC ETFs, cash; in some jurisdictions, coins) to the fund and receives newly minted shares that it sells into the market. When shares trade at a discount, the AP does the reverse. The AP is not doing this as a favor; the spread between market price and NAV is its arbitrage margin.

Only a small number of firms are approved APs for any given fund, and the overlap across funds is heavy. The same handful of desks are making markets in IBIT, FBTC, and now the HYPE products. This is not accidental — the operational, credit, and compliance requirements to be an AP are steep — but it does concentrate market-making risk in ways worth naming.

The custodian

The custodian holds the actual private keys. For the majority of U.S. spot bitcoin ETFs, that custodian is Coinbase Custody Trust Company, a New York-chartered limited-purpose trust. Fidelity uses its own in-house custody arm, and a few smaller funds spread across BitGo, Anchorage, or Gemini. But the market share concentration in Coinbase is unusual for a mature financial product category and deserves its own section, below.

The custodian’s job is bounded: receive coins when creations happen, release coins when redemptions happen, keep the rest in cold storage, and produce attestations. The custodian does not trade, hedge, or lend the coins under the standard ETF agreements — a distinction from prime brokerage arrangements in traditional finance.

The market maker and the exchange

The market maker — often the same firm as the AP, wearing a different hat — provides continuous two-sided quotes on the listed exchange (typically NYSE Arca, Cboe BZX, or Nasdaq). The exchange itself provides the matching engine, surveillance, and the SEC-registered venue that allows the shares to be sold to retail and to sit in tax-advantaged accounts.

The end investor interacts only with the last two layers: they buy a share on an exchange from a market maker. Everything else — the sponsor’s contract with the custodian, the AP’s creation basket, the movement of coins into cold storage — happens invisibly upstream.

Custody concentration and the Coinbase question

The most-cited structural feature of the U.S. spot bitcoin ETF cohort is that a large majority of the underlying coins sit with a single custodian: Coinbase Custody. Public 10-K and prospectus disclosures from most of the major sponsors — including BlackRock, Grayscale, Bitwise, Ark 21Shares, VanEck, and Invesco Galaxy — name Coinbase as the custodian at launch. Fidelity is the notable large exception, using Fidelity Digital Asset Services.

This concentration has three consequences worth examining separately: operational risk, market structure risk, and reflexive lending risk.

Operational risk

Coinbase Custody operates as a New York State-chartered trust company, subject to NYDFS supervision, and holds assets in bankruptcy-remote structures separate from Coinbase Inc.’s operating balance sheet. In principle, a Coinbase Global bankruptcy should not commingle ETF assets with creditor claims. In practice, this has never been tested at the scale of the current custody book, and the legal literature on bankruptcy-remote crypto custody remains thin. Sponsor prospectuses generally acknowledge this uncertainty in their risk factors.

The operational surface — signing infrastructure, personnel, physical facilities, HSMs — is also singular. A serious operational incident at Coinbase Custody would touch a majority of listed U.S. spot BTC AUM simultaneously. There is no obvious analogue in traditional finance where a single sub-custodian holds this share of a broadly-marketed asset class.

Market structure risk

Coinbase is also the largest U.S. regulated spot exchange and, through its surveillance-sharing agreement with the listing exchanges, is the reference market that provided the “regulated market of significant size” argument the SEC eventually accepted for spot bitcoin approval. The same entity is thus (a) the custodian, (b) a major spot venue whose prices influence NAV calculations via index providers, and (c) a public company whose equity is itself a listed instrument.

None of these roles is per se conflicted, and each is walled off in separate legal entities. But the consolidation of custody, price discovery, and surveillance in one corporate family is a structural feature that would not be tolerated in most other listed markets.

Lending and rehypothecation

Under the current ETF agreements we are aware of, the custodian does not lend the coins. This distinguishes the wrapper from prime brokerage or from unregulated crypto lenders whose 2022 failures did involve rehypothecation. If a future sponsor amends its trust agreement to permit yield generation on idle coins — an obvious commercial temptation — the risk profile of the shares changes materially. Readers of any prospectus should check the custody and lending sections directly rather than assuming the current no-lending posture is permanent.

Creation, redemption, and the arbitrage that keeps price honest

The reason ETF shares track NAV closely — historically within a few basis points for the largest U.S. spot BTC products — is not that the fund promises a peg. It is that a small group of professional arbitrageurs are contractually positioned to profit from any deviation.

The mechanical loop

Consider a simplified creation cycle. Suppose one ETF share represents 0.0001 BTC. If the ETF trades on the exchange at a price implying 0.00011 BTC per share while spot bitcoin sits at the lower reference, an AP can:

- Buy spot bitcoin at the reference price, either on Coinbase or across a basket of venues.

- Deliver either that bitcoin or an equivalent cash amount (depending on the fund’s creation model) to the sponsor, along with any applicable fee.

- Receive a block of newly issued ETF shares — typically in creation units of 10,000 or more shares.

- Sell those shares into the market at the elevated price.

The AP pockets the spread, minus transaction costs and financing. The act of buying spot pushes reference price up; the act of selling new shares pushes ETF price down; the two converge. Redemptions run the loop in reverse when shares trade at a discount.

Cash creates versus in-kind creates

A subtle but consequential U.S.-specific detail: the SEC required spot bitcoin ETFs at launch to use cash creation and redemption rather than in-kind. Under cash creates, the AP delivers dollars, and the sponsor (through an agent, often the custodian’s execution desk or a designated trading agent) buys the bitcoin. Under in-kind, the AP would deliver bitcoin directly.

Cash creates simplify the AP’s regulatory position — the AP itself never has to hold, transfer, or touch crypto — which was central to getting broker-dealers comfortable. The tradeoff is that the sponsor bears execution risk in the interval between accepting cash and acquiring coins, and that spread is passed to shareholders in the form of slightly wider tracking error and slightly higher transaction cost drag versus a hypothetical in-kind structure. Proposals to move some products to in-kind creation have circulated; the mechanics are worth watching because they reduce a source of frictional cost.

What happens when arbitrage breaks

The arbitrage is not unconditional. It relies on APs being able to (a) source or offload spot inventory, (b) finance the position between creation and settlement, and (c) route orders during the ETF’s trading hours. Each of these can fail in specific ways.

If the underlying spot market gaps — a weekend BTC move outside U.S. trading hours is the canonical case — the ETF opens Monday with a discovery gap that the AP cannot arbitrage away instantly, because they can only create or redeem on a T+1 or T+2 settlement schedule while the exchange price moves in real time. Small premium/discount excursions have been observed at every fund. During the March 2020-style stress in traditional markets, fixed-income ETFs traded at 5% discounts to stated NAV for days because APs could not source underlying inventory at the reference; a large-scale crypto equivalent has not yet been observed in the spot ETF era, but the theoretical fragility is real.

If a specific AP steps back — for credit reasons, for compliance reasons, for internal risk-limit reasons — the remaining APs must absorb creation demand. The Grayscale GBTC discount that persisted for over a year before its ETF conversion is not an exact analogue (GBTC was closed-end at the time, with no redemption mechanism at all), but it illustrates how quickly the wrapper’s price can decouple when the arbitrage channel is impaired.

What the HYPE launch shows about the template

The spot HYPE ETFs that launched in late 2025 provide a fresh datapoint for how quickly the wrapper template now extends to newer assets. Reported early volume approached $900M in the initial trading window, a figure that, if the reporting is accurate, would be strong even by the standards of the January 2024 spot BTC launches — which themselves broke ETF launch records.

Two observations sit under this number.

The distribution channel does the heavy lifting

The HYPE token itself is a governance and gas asset for a specific derivatives-focused L1. Its holder base pre-ETF was concentrated in on-chain participants who had no obvious need for a listed wrapper. The volume in the first days of trading was therefore, largely by construction, new money — investors who could not or would not hold the underlying directly.

This confirms what the bitcoin ETFs demonstrated in aggregate over their first two years: the wrapper does not primarily convert existing holders. It reaches an adjacent pool — RIAs, brokerage accounts, retirement vehicles, corporate treasuries with mandates that require SEC-registered securities. The question of whether a given asset “deserves” an ETF collapses into a narrower question: is there enough distribution appetite to justify the sponsor’s operating cost.

The template is now standardized

The HYPE products launched with roughly the same architecture as the BTC and ETH funds: cash creates, familiar sponsors, familiar APs, and — for at least some issuers — Coinbase Custody as sub-custodian. The path from “novel asset” to “listed spot ETF” has compressed from years (for BTC) to what appears to be months for subsequent assets, assuming a workable index and a listing exchange willing to file the required 19b-4.

The standardization is good for launch speed and bad for structural diversity. Every incremental spot crypto ETF added to the U.S. market inherits the same custody concentration, the same cash-create limitation, and the same handful of APs. Systemic exposure to any single point of failure — the largest custodian, the largest AP, the reference exchange — grows with each product.

What bitcoin loses inside the wrapper

The Trezor executive’s critique — that the ETF format is the worst outcome for bitcoin — is easy to dismiss as hardware-wallet incumbency talking its book. It deserves a more careful reading. The argument, stripped of rhetorical flourish, is that the properties that distinguish bitcoin from a bearer share of any commodity trust are precisely the properties that the wrapper strips away. Whether that matters depends on why one holds the asset.

Self-custody and censorship resistance

An ETF shareholder does not hold bitcoin. They hold a claim on a trust that holds bitcoin, and that claim is denominated in a share tradable on a registered exchange during specified hours. The custodian’s compliance policies — sanctions screening, transaction monitoring, jurisdictional restrictions — sit between the shareholder and the underlying asset by design. This is not a defect of the ETF; it is the reason the ETF was approvable.

If the reason for holding bitcoin is exposure to its dollar price, this distinction is immaterial. If the reason is any of the properties that flow from unilateral control of a bearer instrument — the ability to transact without permission, to hold outside any single legal jurisdiction, to be censorship-resistant against a specific state action — those properties do not survive the wrapper. The ETF shareholder is, in every meaningful sense, an equity holder in a specialized trust, with all the state-mediated protections and constraints that entails.

24/7 settlement collapses to T+1 with trading hours

Bitcoin’s base layer settles blocks continuously, weekends and holidays included. ETF shares settle T+1 through DTCC and trade only during exchange hours. A holder who wants to reposition on a Sunday morning cannot, regardless of what the underlying is doing. The wrapper imposes the settlement calendar of 1970s equities on an asset whose defining feature was breaking that calendar.

For most investors, this is a non-issue; institutional flow does not typically care about Sunday liquidity. For the specific subset of holders who valued 24/7 settlement — market makers, cross-border remitters, treasuries that needed weekend optionality — the ETF is not a substitute for direct ownership.

Governance and forks

An ETF shareholder has no voice in chain-level governance events. If a contentious hard fork occurs, the sponsor decides which side of the fork the trust holds and whether to distribute, sell, or ignore the forked asset. The 2017 SegWit2x and Bitcoin Cash episodes would look very different if the majority of institutional BTC exposure sat inside trust structures with prospectus-defined fork policies. This is not hypothetical for smaller-cap assets: any future contentious governance decision in a wrapped asset’s underlying chain is now partially delegated to sponsors and their custodians.

Fee drag

ETFs charge expense ratios. Current spot BTC ETF fees range from around 0.15% to 0.25% for the price-competitive tier, with older or specialty products charging more. Over a long holding period this compounds meaningfully against a self-custodied position that pays only one-time transaction and custody costs. The fee is not unreasonable given the operational cost of running the fund; it is simply a real cost that does not exist for direct holders.

What is gained

None of this is to dismiss what the wrapper adds. Auditability, standard tax reporting, integration with existing portfolio infrastructure, protection against user-side custody errors (the largest single category of historical bitcoin loss), and — for regulated pools of capital — the ability to hold the asset at all. For an endowment or pension fund, the ETF is not a compromise; it is the only compliant path to exposure. The Trezor critique is not that these benefits do not exist. It is that framing them as strictly additive misses the tradeoff on the other side of the ledger.

What to watch from here

Several structural questions will shape the next phase of the spot crypto ETF market, and each is worth monitoring on its own terms.

Custody diversification. Whether the concentration in Coinbase Custody unwinds — through the addition of secondary custodians to existing funds, or through new products launching with different arrangements — is the single most important structural risk variable. Any regulatory or operational incident that affects the dominant custodian will be a stress test the market has not yet seen.

In-kind creation. If the SEC allows a shift to in-kind creation and redemption for spot crypto ETFs, tracking error should tighten and the AP set may broaden as broker-dealers become willing to touch the underlying directly. This is a purely mechanical change with real cost implications for shareholders.

Rehypothecation drift. The current no-lending posture in ETF custody agreements is a design choice, not a regulatory floor. Watch for sponsors amending trust agreements to permit staking (in the case of PoS assets), lending, or other yield generation on idle coins. Each such amendment changes the risk profile of the shares in ways that fee comparisons alone will not capture.

AP concentration and stress behavior. The current AP set for spot crypto ETFs overlaps heavily with the AP set for the largest fixed-income and equity ETFs. In a genuine market stress event, capital and risk appetite at these desks is not additive across product lines. The behavior of premiums and discounts during the next macro shock will be more informative about the wrapper’s robustness than anything visible in current calm-market tracking data.

Governance delegation. As more assets are wrapped — particularly proof-of-stake assets with active governance — the question of how sponsors handle chain-level decisions becomes material. A concentration of voting or staking authority in the hands of a small set of ETF sponsors and their custodians is a governance concentration that on-chain communities have not fully absorbed.

The wrapper is neither the salvation of crypto nor its worst outcome. It is a specific piece of financial plumbing with specific tradeoffs, and the honest analytical posture is to understand those tradeoffs rather than adopt them or reject them wholesale. What the ETF gives — distribution, compliance, integration — is real. What it takes — self-custody, 24/7 settlement, governance participation, censorship resistance — is also real. Whether the trade is worth making is a question that depends entirely on why one wanted the underlying asset in the first place.

서론

이 글이 답하려는 질문을 압축하는 두 가지 데이터 포인트가 2025년 말에 등장했다. 첫째, 현물 HYPE ETF가 미국에서 출시되어 첫날 거래량이 약 9억 달러에 달했다는 보도가 나왔다. 이는 현물 BTC와 ETH 상품이 세운 패턴의 연장선이다. 새로 상장되는 암호화폐 래퍼마다 기관 자금이 수 시간 안에 유입된다. 둘째, 하드웨어 지갑 제조사 Trezor의 고위 임원은 ETF 형태가 비트코인에게 “최악의 결과”라고 공개적으로 주장했다. 접근성은 높아지지만, 그 자산을 가질 만하게 만들었던 본질적 속성이 텅 비어버린다는 논리였다.

두 주장 모두 사실일 수 있다. ETF 래퍼는 암호화폐가 지금껏 활용한 배포 메커니즘 중 가장 성공적인 것이다. 동시에 보유자가 실질적으로 소유하는 것을 구조적으로 변형시킨다. 한쪽의 마케팅 수사와 다른 쪽의 이념적 거부 사이에는, 대부분의 보도가 건너뛰는 배관 공학적 질문들이 자리한다. 실제로 누가 코인을 보유하는가, 주식 가격은 어떻게 현물 가격에 연동되는가, 스트레스 상황에서는 무슨 일이 벌어지는가, 비트코인의 원래 속성 중 래핑 이후에도 살아남는 것은 무엇인가.

이 글은 바로 그 배관을 들여다본다. 스폰서, 공인 참여자(AP), 커스터디언, 마켓 메이커를 연결하는 4자 구조, 단일 미국 기관에 집중된 핵심 커스터디, 순자산가치(NAV)를 촘촘하게 유지하는 차익거래 메커니즘, 그리고 ETF 주식을 보유한다는 것이 암묵적으로 수반하는 법적·운영적·철학적 트레이드오프를 살펴본다. HYPE 출시와 Trezor 비판은 현재의 닻 역할을 하지만, 구조적 질문은 현재 거래 중이거나 승인을 기다리는 모든 현물 암호화폐 ETF에 동일하게 적용된다.

모든 현물 암호화폐 ETF 안의 네 당사자

현물 암호화폐 ETF는 흔히 수동적 컨테이너처럼 묘사된다. 코인이 들어가고, 주식이 나오고, 가격이 따라간다는 식으로. 실제로는 각자의 유인 구조와 고장 지점을 가진 네 개의 별개 법인이 펼치는 정교한 협력의 춤이다.

스폰서

스폰서는 — IBIT의 BlackRock, FBTC의 Fidelity, BITB 상품의 Bitwise 등 — 펀드의 발행사이자 마케터다. 스폰서는 투자설명서를 작성하고, 수수료율을 설정하고, 커스터디언을 고용하며, 자산에서 운용 수수료를 가져간다. 그러나 스폰서는 코인을 직접 보유하지 않는다. 창고 운영자보다는 총괄 시공자에 가깝다.

스폰서의 핵심 자산은 배포 관계망이다. 브로커리지 플랫폼 통합, 재무설계사 커버리지, 지수 편입, 그리고 국가 증권거래소에 상장할 수 있는 규제 승인이 그것이다. 이 배포 레일은 자기 수탁(self-custody) 비트코인이 접근할 수 없는 영역이며, ETF가 상업적으로 존재하는 이유의 전부다.

공인 참여자

공인 참여자(AP, Authorized Participant)는 이 구조의 기계적 심장이다. AP는 일반적으로 대형 브로커-딜러들이다. 미국 시장에서는 Jane Street, Virtu, Cantor Fitzgerald, JPMorgan의 증권 부문, 그리고 소수의 다른 회사들이 펀드와 직접 주식을 설정·환매할 수 있는 계약상 권리를 보유한다.

ETF 주식에 대한 최종 투자자 수요가 NAV 대비 프리미엄을 형성하면, AP는 해당 바스켓(현재 미국 현물 BTC ETF에서는 현금, 일부 국가에서는 코인)을 펀드에 납입하고 새로 발행된 주식을 받아 시장에 매도한다. 주식이 할인 거래될 때는 역방향으로 작동한다. AP는 호의로 이 일을 하는 게 아니다. 시장 가격과 NAV 사이의 스프레드가 그들의 차익거래 마진이다.

어떤 특정 펀드에 대해서도 승인된 AP는 소수에 불과하며, 펀드 간 중복은 상당하다. 같은 소수의 데스크들이 IBIT, FBTC, 그리고 이제는 HYPE 상품에도 마켓 메이킹을 한다. 이것은 우연이 아니다. AP가 되기 위한 운영·신용·컴플라이언스 요건이 높기 때문이다. 하지만 이는 마켓 메이킹 리스크를 짚어볼 필요가 있는 방식으로 집중시킨다.

커스터디언

커스터디언은 실제 개인 키를 보관한다. 미국 현물 비트코인 ETF의 대다수는 뉴욕 주법에 따라 설립된 제한적 목적 신탁인 Coinbase Custody Trust Company를 커스터디언으로 사용한다. Fidelity는 자체 커스터디 부문을 사용하고, 소수의 소형 펀드는 BitGo, Anchorage, Gemini에 분산되어 있다. 그러나 Coinbase에 대한 시장 점유율 집중은 성숙한 금융 상품 범주에서는 이례적이며, 이는 별도로 다룰 가치가 있다.

커스터디언의 역할은 한정적이다. 설정 시 코인을 수령하고, 환매 시 코인을 내보내고, 나머지는 콜드 스토리지에 보관하며, 증명서를 발행하는 것이다. 커스터디언은 표준 ETF 계약 하에서 코인을 거래하거나, 헤지하거나, 대여하지 않는다. 이는 전통 금융의 프라임 브로커리지 약정과 구별되는 중요한 차이점이다.

마켓 메이커와 거래소

마켓 메이커는 — 흔히 다른 역할을 수행하는 AP와 동일한 회사다 — 상장 거래소(일반적으로 NYSE Arca, Cboe BZX, 또는 Nasdaq)에서 지속적인 양방향 호가를 제공한다. 거래소 자체는 매칭 엔진, 시장 감시, 그리고 주식을 리테일에 판매하고 세금 혜택 계좌에 편입할 수 있게 해주는 SEC 등록 거래 장소를 제공한다.

최종 투자자는 마지막 두 레이어와만 상호작용한다. 거래소에서 마켓 메이커로부터 주식을 매수하는 것이다. 그 밖의 모든 것, 즉 스폰서의 커스터디언과의 계약, AP의 설정 바스켓, 코인의 콜드 스토리지 이동은 투자자 눈에 보이지 않는 상류에서 처리된다.

커스터디 집중과 Coinbase 문제

미국 현물 비트코인 ETF 군에서 가장 많이 언급되는 구조적 특징은, 기초 코인의 상당 부분이 단일 커스터디언인 Coinbase Custody에 집중되어 있다는 점이다. BlackRock, Grayscale, Bitwise, Ark 21Shares, VanEck, Invesco Galaxy를 포함한 대부분의 주요 스폰서가 제출한 10-K와 투자설명서는 출시 시점의 커스터디언으로 Coinbase를 명시하고 있다. Fidelity는 자체 Fidelity Digital Asset Services를 사용하는 주목할 만한 대형 예외다.

이 집중화는 별도로 검토할 가치가 있는 세 가지 결과를 초래한다. 운영 리스크, 시장 구조 리스크, 그리고 반사적 대출 리스크가 그것이다.

운영 리스크

Coinbase Custody는 뉴욕주 인가 신탁회사로 NYDFS의 감독을 받으며, Coinbase Inc.의 영업 대차대조표와 분리된 도산 격리 구조로 자산을 보관한다. 원칙적으로는, Coinbase Global이 파산하더라도 ETF 자산이 채권자 청구와 혼합되어서는 안 된다. 실제로는, 이것이 현재 커스터디 장부 규모에서 한 번도 검증된 적이 없으며, 도산 격리 암호화폐 커스터디에 관한 법적 문헌도 여전히 빈약하다. 스폰서의 투자설명서는 대체로 이 불확실성을 위험 요소에서 인정하고 있다.

서명 인프라, 인력, 물리적 시설, HSM 등 운영 표면 역시 단일하다. Coinbase Custody에서 심각한 운영 사고가 발생하면, 상장된 미국 현물 BTC 운용자산(AUM)의 대부분이 동시에 영향을 받는다. 전통 금융에서 단일 서브 커스터디언이 광범위하게 마케팅된 자산 클래스의 이 정도 비중을 보유하는 유사한 사례는 찾기 어렵다.

시장 구조 리스크

Coinbase는 또한 미국 최대 규제 현물 거래소이며, 상장 거래소와의 시장 감시 공유 협정을 통해, SEC가 현물 비트코인 승인에 결국 수용한 “상당한 규모의 규제된 시장” 논거를 제공한 기준 시장이기도 하다. 따라서 동일한 법인이 (a) 커스터디언이자, (b) 인덱스 제공업체를 통한 NAV 계산에 영향을 미치는 주요 현물 거래소이자, (c) 그 자체가 상장된 주식인 상장 기업이다.

이 각각의 역할이 그 자체로 이해 충돌을 의미하는 것은 아니며, 별도의 법인으로 분리되어 있다. 그러나 커스터디, 가격 발견, 감시가 하나의 기업 집단에 통합된 것은, 다른 대부분의 상장 시장에서라면 용인되지 않을 구조적 특징이다.

대출과 재담보화

현재 우리가 파악하고 있는 ETF 계약 하에서, 커스터디언은 코인을 대출하지 않는다. 이 점이 이 래퍼를 프라임 브로커리지, 또는 2022년 파산 사태에서 재담보화가 실제로 이루어진 비규제 암호화폐 대출업체들과 구별 짓는다. 만약 미래의 스폰서가 신탁 계약을 개정하여 유휴 코인에 대한 수익률 창출을 허용한다면 — 상업적으로 명백한 유혹이다 — 주식의 리스크 프로파일은 상당히 달라진다. 어떤 투자설명서를 읽든, 현재의 무대출 방침이 영구적이라고 가정하지 말고 커스터디 및 대출 조항을 직접 확인해야 한다.

설정, 환매, 그리고 가격을 정직하게 유지하는 차익거래

ETF 주식이 NAV를 촘촘하게 추적하는 이유 — 역사적으로 미국 최대 현물 BTC 상품들의 경우 수 베이시스 포인트 이내 — 는 펀드가 연동을 약속했기 때문이 아니다. 소수의 전문 차익거래자들이 어떤 이탈에서도 계약상 수익을 얻도록 포지셔닝되어 있기 때문이다.

기계적 순환 구조

단순화된 설정 사이클을 생각해보자. ETF 주식 1주가 0.0001 BTC를 나타낸다고 하자. 만약 ETF가 거래소에서 주당 0.00011 BTC에 해당하는 가격에 거래되는 반면 현물 비트코인이 더 낮은 기준가에 있다면, AP는 다음을 실행할 수 있다.

- Coinbase 또는 여러 거래소 바스켓에서 기준 가격에 현물 비트코인을 매수한다.

- 해당 비트코인 또는 동등한 현금(펀드의 설정 모델에 따라)을 수수료와 함께 스폰서에게 납입한다.

- 새로 발행된 ETF 주식 블록 — 일반적으로 설정 단위 10,000주 이상 — 을 수령한다.

- 상승된 가격에 해당 주식을 시장에 매도한다.

AP는 거래 비용과 파이낸싱 비용을 제한 스프레드를 수취한다. 현물 매수 행위가 기준 가격을 밀어 올리고, 신규 주식 매도 행위가 ETF 가격을 끌어내리며, 두 가격은 수렴한다. 환매는 주식이 할인 거래될 때 역방향으로 이 순환을 반복한다.

현금 설정 vs. 현물 설정

미국 특유의 미묘하지만 중요한 세부 사항이 있다. SEC는 출시 시점에 현물 비트코인 ETF가 현물이 아닌 현금 설정·환매 방식을 사용하도록 요구했다. 현금 설정 방식에서는 AP가 달러를 납입하고, 스폰서가 (흔히 커스터디언의 실행 데스크나 지정 거래 대리인을 통해) 비트코인을 매수한다. 현물 설정이라면 AP가 비트코인을 직접 납입했을 것이다.

현금 설정은 AP의 규제적 입장을 단순화한다. AP 자체가 암호화폐를 보유·이전하거나 접촉할 필요가 없어, 브로커-딜러들이 참여하는 데 핵심적이었다. 트레이드오프는 스폰서가 현금을 수령하고 코인을 취득하는 사이 실행 리스크를 부담한다는 것이며, 이 스프레드는 가상의 현물 설정 구조 대비 약간 더 넓은 추적 오차와 약간 더 높은 거래 비용 마찰로 주주에게 전가된다. 일부 상품을 현물 설정으로 전환하자는 제안이 제기된 바 있으며, 이는 마찰 비용을 줄이는 방향이므로 동향을 주시할 가치가 있다.

차익거래가 작동하지 않을 때

차익거래는 무조건적이지 않다. 이것은 AP가 (a) 현물 재고를 조달하거나 매도하고, (b) 설정과 결제 사이에 포지션을 파이낸싱하며, (c) ETF 거래 시간 중 주문을 처리할 수 있다는 전제에 의존한다. 이 각각은 특정한 방식으로 실패할 수 있다.

기초 현물 시장이 급등락하면 — 미국 거래 시간 외 주말 BTC 변동이 대표적인 사례다 — ETF는 월요일에 AP가 즉시 차익거래할 수 없는 가격 발견 갭을 안고 개장한다. 거래소 가격이 실시간으로 움직이는 동안 설정·환매는 T+1 또는 T+2 결제 일정에 따라서만 가능하기 때문이다. 소규모의 프리미엄·할인 이탈은 모든 펀드에서 관찰된 바 있다. 2020년 3월의 전통 시장 스트레스 상황에서, 채권 ETF들은 며칠 동안 명시된 NAV 대비 5% 할인에 거래되었는데, AP가 기준 가격에 기초 자산을 조달할 수 없었기 때문이다. 현물 ETF 시대에 암호화폐 등가 사태는 아직 관찰된 적 없지만, 이론적 취약성은 실재한다.

특정 AP가 신용 문제, 컴플라이언스 문제, 내부 리스크 한도 문제로 물러서면, 나머지 AP들이 설정 수요를 흡수해야 한다. 1년 이상 지속된 Grayscale GBTC의 할인은 정확한 유사 사례는 아니다 — GBTC는 당시 환매 메커니즘이 전혀 없는 폐쇄형 구조였다 — 그러나 차익거래 채널이 손상되었을 때 래퍼 가격이 얼마나 빠르게 이탈할 수 있는지를 보여준다.

HYPE 출시가 이 템플릿에 대해 보여주는 것

2025년 말 출시된 현물 HYPE ETF는 이 래퍼 템플릿이 얼마나 빠르게 신규 자산으로 확장되는지에 대한 신선한 데이터 포인트를 제공한다. 초기 거래 구간에서 보고된 초기 거래량은 약 9억 달러에 달했는데, 이 수치가 정확하다면 ETF 출시 기록을 자체적으로 경신한 2024년 1월 현물 BTC 출시의 기준으로 봐도 상당한 수치다.

이 숫자 아래에는 두 가지 관찰이 자리한다.

배포 채널이 핵심 역할을 한다

HYPE 토큰 자체는 특정 파생상품 중심 레이어 1의 거버넌스 및 가스 자산이다. ETF 출시 전 보유자 기반은 상장 래퍼가 명백히 필요하지 않은 온체인 참여자들에 집중되어 있었다. 따라서 초기 거래 첫 며칠간의 거래량은, 구조적으로, 대부분 신규 자금이었다. 기초 자산을 직접 보유할 수 없거나 보유하지 않으려는 투자자들의 자금 말이다.

이것은 비트코인 ETF들이 첫 2년간 총체적으로 증명한 것을 확인해준다. 래퍼는 주로 기존 보유자를 전환하지 않는다. 인접한 풀, 즉 SEC 등록 증권을 요구하는 위임장을 가진 투자자문사(RIA), 브로커리지 계좌, 은퇴 저축 수단, 기업 자금을 새로 끌어들인다. 특정 자산이 ETF를 “받을 자격이 있는가”라는 질문은 더 좁은 질문으로 귀결된다. 스폰서의 운영 비용을 정당화할 만큼 충분한 배포 수요가 있는가.

템플릿은 이제 표준화되었다

HYPE 상품들은 BTC 및 ETH 펀드와 거의 동일한 구조로 출시되었다. 현금 설정, 익숙한 스폰서들, 익숙한 AP들, 그리고 최소한 일부 발행사의 경우 서브 커스터디언으로 Coinbase Custody. “신규 자산”에서 “상장 현물 ETF”에 이르는 경로는 BTC의 경우 수년에서, 실행 가능한 인덱스와 필요한 19b-4를 제출할 의향이 있는 상장 거래소만 있다면, 후속 자산의 경우 몇 달로 압축된 것으로 보인다.

표준화는 출시 속도 측면에서는 좋지만, 구조적 다양성 측면에서는 나쁘다. 미국 시장에 추가되는 모든 현물 암호화폐 ETF는 동일한 커스터디 집중, 동일한 현금 설정 한계, 동일한 소수의 AP를 상속한다. 단일 장애점 — 최대 커스터디언, 최대 AP, 기준 거래소 — 에 대한 시스템적 노출은 상품이 추가될수록 커진다.

비트코인이 래퍼 안에서 잃는 것

Trezor 임원의 비판 — ETF 형태가 비트코인에게 최악의 결과라는 주장 — 은 하드웨어 지갑 기득권이 자신의 이익을 대변하는 것으로 쉽게 일축할 수 있다. 하지만 더 신중하게 읽을 필요가 있다. 수사적 과장을 걷어낸 그 주장의 핵심은, 비트코인을 단순한 상품 신탁의 무기명 주식과 구별 짓는 속성들이 바로 래퍼가 제거하는 것들이라는 점이다. 이것이 중요한지 여부는 왜 그 자산을 보유하는지에 달려 있다.

자기 수탁과 검열 저항성

ETF 주주는 비트코인을 보유하지 않는다. 그들은 비트코인을 보유한 신탁에 대한 청구권을 보유하며, 그 청구권은 지정된 시간 동안 등록 거래소에서 거래 가능한 주식으로 표시된다. 커스터디언의 컴플라이언스 정책 — 제재 심사, 거래 모니터링, 지역 제한 — 이 설계상 주주와 기초 자산 사이에 위치한다. 이것은 ETF의 결함이 아니다. 오히려 ETF가 승인 가능했던 이유다.

비트코인을 보유하는 이유가 달러 가격 익스포저라면, 이 구분은 무의미하다. 만약 그 이유가 무기명 증서의 일방적 통제에서 비롯되는 속성들 — 허가 없이 거래하는 능력, 단일 법적 관할권 밖에서 보유하는 능력, 특정 국가 행위에 대한 검열 저항성 — 이라면, 그 속성들은 래퍼에서 살아남지 못한다. ETF 주주는 모든 실질적 의미에서 특수 목적 신탁의 지분 보유자이며, 여기에는 국가가 매개하는 모든 보호와 제약이 따른다.

24/7 결제가 거래 시간이 있는 T+1로 축소된다

비트코인의 베이스 레이어는 주말과 공휴일을 포함해 지속적으로 블록을 결제한다. ETF 주식은 DTCC를 통해 T+1로 결제되고, 거래소 거래 시간에만 거래된다. 일요일 아침에 포지션을 재조정하고 싶은 보유자는, 기초 자산이 어떻게 움직이든 상관없이, 그럴 수 없다. 래퍼는 자신의 정의적 특징이 바로 그 달력을 타파하는 것이었던 자산에 1970년대 주식의 결제 달력을 부과한다.

대부분의 투자자에게 이것은 문제가 아니다. 기관 자금은 일반적으로 일요일 유동성에 신경 쓰지 않는다. 24/7 결제를 가치 있게 여겼던 특정 보유자 집단 — 마켓 메이커, 국경간 송금업자, 주말 옵션이 필요한 자금 담당자 — 에게는 ETF가 직접 소유의 대체제가 아니다.

거버넌스와 포크

ETF 주주는 체인 수준의 거버넌스 이벤트에 목소리가 없다. 논쟁적인 하드 포크가 발생하면, 스폰서가 신탁이 어느 쪽 포크를 보유할지, 포크된 자산을 배분·매도·무시할지를 결정한다. 2017년의 SegWit2x와 비트코인 캐시 사태는, 기관의 BTC 익스포저 대부분이 투자설명서에 정의된 포크 정책을 가진 신탁 구조 안에 있었다면 매우 다른 양상을 띠었을 것이다. 이것은 소형 자산에서 가상의 이야기가 아니다. 래핑된 자산의 기초 체인에서 미래에 일어날 논쟁적인 거버넌스 결정은 이제 부분적으로 스폰서와 그들의 커스터디언에게 위임되어 있다.

수수료 마찰

ETF는 운용 수수료를 부과한다. 현재 현물 BTC ETF 수수료는 가격 경쟁 티어의 경우 약 0.15%~0.25%이며, 오래된 상품이나 특수 상품은 더 높다. 장기 보유 기간에 걸쳐 이것은 단회성 거래 및 커스터디 비용만 부담하는 자기 수탁 포지션 대비 의미 있게 복리로 불어난다. 수수료가 펀드 운영 비용을 고려하면 불합리하지 않다. 그것은 단지 직접 보유자에게는 존재하지 않는 실질적인 비용일 뿐이다.

얻는 것

이것이 래퍼가 더하는 것을 부정하려는 게 아니다. 감사 가능성, 표준화된 세금 보고, 기존 포트폴리오 인프라와의 통합, 사용자 측 커스터디 오류로부터의 보호(역사적 비트코인 손실의 단일 최대 범주), 그리고 규제된 자본 풀의 경우 그 자산을 아예 보유할 수 있게 되는 것이 그것이다. 기금이나 연기금에게 ETF는 타협안이 아니다. 그것은 익스포저에 대한 유일한 컴플라이언스 경로다. Trezor의 비판은 이러한 이점들이 존재하지 않는다는 것이 아니다. 그것들을 순전히 가산적인 것으로 프레이밍하는 것이 장부의 반대쪽 트레이드오프를 놓친다는 것이다.

앞으로 주시해야 할 것들

현물 암호화폐 ETF 시장의 다음 단계를 형성할 몇 가지 구조적 질문들이 있으며, 각각은 독자적으로 모니터링할 가치가 있다.

커스터디 다양화. Coinbase Custody에 대한 집중이 해소되는지 — 기존 펀드에 2차 커스터디언이 추가되거나, 다른 약정으로 신규 상품이 출시됨으로써 — 는 단일 가장 중요한 구조적 리스크 변수다. 지배적 커스터디언에 영향을 미치는 규제적 또는 운영적 사고는 시장이 아직 경험하지 못한 스트레스 테스트가 될 것이다.

현물 설정. SEC가 현물 암호화폐 ETF에 대한 현물 설정·환매로의 전환을 허용하면, 추적 오차가 줄어들고 브로커-딜러들이 기초 자산에 직접 접촉할 용의가 생기면서 AP 집합이 넓어질 수 있다. 이것은 주주에게 실질적인 비용 함의를 지닌 순전히 기계적인 변화다.

재담보화 표류. ETF 커스터디 계약의 현재 무대출 방침은 설계적 선택이지, 규제적 하한선이 아니다. 스폰서가 신탁 계약을 개정하여 스테이킹(PoS 자산의 경우), 대출, 또는 유휴 코인에 대한 기타 수익률 창출을 허용하는지 주시하라. 그러한 각각의 개정은 수수료 비교만으로는 포착할 수 없는 방식으로 주식의 리스크 프로파일을 변화시킨다.

AP 집중과 스트레스 상황에서의 행태. 현재 현물 암호화폐 ETF의 AP 집합은 최대 채권 및 주식 ETF의 AP 집합과 상당 부분 겹친다. 진정한 시장 스트레스 이벤트 상황에서, 이 데스크들의 자본과 리스크 감수 능력은 상품 라인 전반에 걸쳐 가산적이지 않다. 다음 거시 충격 시 프리미엄·할인의 거동은, 현재의 안정적인 시장 추적 데이터가 보여주는 어떤 것보다도, 래퍼의 견고성에 대해 더 많은 정보를 줄 것이다.

거버넌스 위임. 더 많은 자산이 래핑될수록 — 특히 활발한 거버넌스를 가진 지분증명(PoS) 자산의 경우 — 스폰서가 체인 수준의 결정을 어떻게 처리하는가라는 질문이 중요해진다. 소수의 ETF 스폰서와 그들의 커스터디언 손에 투표권이나 스테이킹 권한이 집중되는 것은, 온체인 커뮤니티가 아직 충분히 흡수하지 못한 거버넌스 집중이다.

래퍼는 암호화폐의 구원도 최악의 결과도 아니다. 그것은 특정한 트레이드오프를 가진 특정한 금융 배관이며, 정직한 분석적 태도는 그 트레이드오프를 통째로 수용하거나 거부하기보다는 이해하는 것이다. ETF가 주는 것 — 배포, 컴플라이언스, 통합 — 은 실재한다. 그것이 가져가는 것 — 자기 수탁, 24/7 결제, 거버넌스 참여, 검열 저항성 — 역시 실재한다. 그 거래가 가치 있는지는 처음부터 그 기초 자산을 원했던 이유가 무엇이냐에 전적으로 달려 있다.

はじめに

本稿が答えようとする問いは、2025年末の二つのデータポイントによって浮き彫りになる。一つ目は、スポット HYPE ETF が米国で初日取引高~$900M に達したと報じられたこと——スポット BTC・ETH 商品が確立したパターンの延長線上にあり、新たな暗号資産ラッパーが上場するたびに機関投資家のフローが数時間以内に流れ込む。二つ目は、ハードウェアウォレットメーカー Trezor の幹部が、ETF という形式はビットコインにとって「最悪の結果」だと公言したこと——アクセシビリティを高める一方で、そもそもその資産が価値を持った根拠となる特性を空洞化させる、という批判だ。

どちらも正しい。ETF というラッパーは、暗号資産がこれまで手にした中で最も成功した流通メカニズムである。同時に、保有者が実際に所有するものを構造的に変質させる仕組みでもある。一方の過剰なマーケティングと、他方のイデオロギー的拒絶のあいだには、大半の報道が素通りしてしまう一連の「配管の問題」がある。コインを実際に誰が保管しているのか、どのようにして株価がスポット価格に連動するのか、ストレスイベントが起きたときに何が起こるのか、そしてビットコインが本来持っていた特性のうちどれがラッパーを通じても生き残るのか——本稿ではそうした配管を丁寧に辿る。スポンサー、認定参加者、カストディアン、マーケットメーカーという四者から成るアーキテクチャ、米国の単一拠点への鍵管理の集中、純資産価値を一定範囲に保つ裁定メカニズム、そしてETFの株式を保有することで暗黙のうちに受け入れることになるトレードオフ——法的・運営的・哲学的観点から順に見ていく。HYPE の上場と Trezor の批判は現代的な参照点として機能するが、構造的な問いは現在取引されているあらゆるスポット暗号資産 ETF、そして承認待ちのあらゆる商品にも等しく当てはまる。

スポット暗号資産 ETF の内側にある四者構造

スポット暗号資産 ETF はしばしば受動的なコンテナのように語られる——コインを入れると株式が出てきて、価格が連動する、と。しかし実態は、それぞれ異なるインセンティブと障害点を持つ四つの独立した法的主体による、精緻に調整されたダンスだ。

スポンサー

スポンサー——IBIT における BlackRock、FBTC における Fidelity、BITB における Bitwise など——はファンドの発行体かつマーケターだ。スポンサーは目論見書を作成し、経費率を設定し、カストディアンを雇用し、資産から運用報酬を受け取る。ただし、スポンサー自身がコインを保有することはない。倉庫番というよりも、ゼネコンに近い存在だ。

スポンサーの中核的な資産は流通網との関係にある。証券会社のプラットフォーム連携、ファイナンシャルアドバイザーへのカバレッジ、インデックスへの採用、そして国内取引所に上場するための規制当局の承認——それらがセルフカストディのビットコインには届かない流通経路であり、ETF が存在する商業的な理由のすべてだ。

認定参加者

認定参加者(AP: Authorized Participant)はこの仕組みの機械的な心臓部だ。AP は通常、大手ブローカー・ディーラーだ——米国市場では Jane Street、Virtu、Cantor Fitzgerald、JPMorgan の証券部門などごく少数の企業が、ファンドと直接株式の設定・解約を行う契約上の権利を持つ。

ETF 株式が NAV を上回るプレミアム状態になると、AP は必要なバスケット(現行の米国スポット BTC ETF では現金で、一部の国・地域ではコインで)をファンドに引き渡し、新規発行された株式を受け取って市場で売却する。株式がディスカウントで取引されている場合は逆の動きをする。AP がこれを行うのは善意からではない。市場価格と NAV の乖離が裁定利益の源泉だ。

特定のファンドに対して承認された AP の数は少なく、各ファンド間での重複は大きい。IBIT、FBTC、そして今回の HYPE 商品でも、同じ少数のデスクがマーケットメイクを担っている。これは偶然ではない——AP となるための運営上・信用上・コンプライアンス上の要件は厳しい——だが、それがマーケットメイクリスクを特定の主体に集中させているという事実は直視する必要がある。

カストディアン

カストディアンが実際の秘密鍵を保管する。米国の大半のスポットビットコイン ETF において、そのカストディアンは Coinbase Custody Trust Company——ニューヨーク州認可の限定目的信託会社——だ。Fidelity は自社のインハウス・カストディ部門を使用しており、一部の小規模ファンドは BitGo、Anchorage、または Gemini に分散している。しかし Coinbase への市場シェア集中は、成熟した金融商品カテゴリーとしては異例であり、後の節で独立して論じる。

カストディアンの役割は明確に限定されている。設定時にコインを受け取り、解約時にコインを返却し、残りをコールドストレージで保管し、残高証明を発行する。標準的な ETF 契約のもとでは、カストディアンはコインのトレード、ヘッジ、貸し出しを行わない——これは従来型金融のプライムブローカレッジ契約との重要な違いだ。

マーケットメーカーと取引所

マーケットメーカー——AP と同一の企業が別の役割を担うことも多い——は上場取引所(通常は NYSE Arca、Cboe BZX、または Nasdaq)で継続的に双方向の気配値を提示する。取引所自体はマッチングエンジン、監視機能、および SEC 登録済みの場を提供し、株式をリテール投資家に販売可能にし、課税優遇口座に組み込めるようにする。

エンドインベスターが関与するのは最後の二層だけだ。取引所でマーケットメーカーから株式を買う、それだけだ。それより上流で起こること——スポンサーとカストディアンの契約、AP の設定バスケット、コインのコールドストレージへの移動——はすべて見えないところで処理されている。

カストディの集中と Coinbase 問題

米国スポットビットコイン ETF コホートの構造的特徴として最も多く引用されるのは、裏付けとなるコインの大多数が単一のカストディアンである Coinbase Custody に集中しているという点だ。BlackRock、Grayscale、Bitwise、Ark 21Shares、VanEck、Invesco Galaxy を含む主要スポンサーの大半が、上場時点のカストディアンとして Coinbase を 10-K や目論見書で開示している。大手の例外として Fidelity は自社の Fidelity Digital Asset Services を使用している。

この集中には独立して検討する価値のある三つの帰結がある。運営リスク、市場構造リスク、そして反射的な貸し出しリスクだ。

運営リスク

Coinbase Custody はニューヨーク州認可の信託会社として NYDFS の監督下に置かれており、資産は Coinbase Inc. の事業バランスシートとは切り離された倒産隔離構造に保有される。原則として、Coinbase Global が破綻しても ETF の資産は債権者の請求と混同されないはずだ。しかしこれは現在の預かり残高規模では実際にテストされたことがなく、倒産隔離型の暗号資産カストディに関する法的先例も乏しい。スポンサーの目論見書はおおむね、このような不確実性をリスク要因として記載している。

署名インフラ、人員、物理的施設、HSM といった運営上の攻撃対象領域も一点集中している。Coinbase Custody で深刻な運営インシデントが発生した場合、上場している米国スポット BTC AUM の大半が同時に影響を受ける。広く販売されている資産クラスの単一のサブカストディアンがこれほどのシェアを持つ例は、従来型金融には明確な類似事例がない。

市場構造リスク

Coinbase は米国最大の規制対象スポット取引所でもある。上場取引所との監視共有協定を通じて、SEC がスポットビットコイン承認の根拠として最終的に受け入れた「相当規模の規制市場」の論拠を提供したのも Coinbase だ。つまり同一の主体が、(a)カストディアン、(b)インデックスプロバイダーを経由して NAV 算出に影響を与える主要スポット会場、(c)上場株式である公開企業、という三役を同時に担っていることになる。

これらの役割はそれぞれそれ自体として利益相反ではなく、いずれも別々の法人によって区画されている。しかし、カストディ、価格発見、監視が単一の企業グループに集中するという構造的特徴は、ほとんどの他の上場市場では容認されないだろう。

貸し出しとリハイポセケーション

現時点で把握している ETF 契約の範囲では、カストディアンはコインを貸し出さない。これは、リハイポセケーションを伴い 2022 年の崩壊を招いた規制外の暗号資産貸し出し業者や、プライムブローカレッジとの明確な違いだ。将来あるスポンサーが信託契約を改定し、遊休コインからの 利回り 生成を認める場合——商業的な誘惑としては明白だ——株式のリスクプロファイルは実質的に変わる。どの目論見書についても、現在の無貸し出しの立場が永続的と仮定せず、カストディと貸し出しに関するセクションを直接確認する習慣を持つべきだ。

設定・解約と価格を適正に保つ裁定

ETF 株式が NAV に緊密に連動する理由——最大手の米国スポット BTC 商品では歴史的に数ベーシスポイント以内——は、ファンドが特定のペッグを約束しているからではない。少数の専門的な裁定業者が、あらゆる乖離から利益を得られるよう契約上の立場を確保しているからだ。

機械的なループ

シンプルな設定サイクルを考えてみよう。ある ETF 株式が 0.0001 BTC を表すとする。ETF が取引所で 1 株あたり 0.00011 BTC に相当する価格で取引される一方、スポットビットコインが参照価格より低い水準にある場合、AP は以下を実行できる。

- Coinbase あるいは複数の取引会場で参照価格のスポットビットコインを買う。

- そのビットコインまたは同等の現金(ファンドの設定モデルによる)に加え、所定の手数料をスポンサーに引き渡す。

- 新規発行の ETF 株式——通常は 10,000 株以上の設定単位——を受け取る。

- その株式を高値で市場に売る。

AP は取引コストと資金調達費用を差し引いたスプレッドを獲得する。スポット買いが参照価格を押し上げ、新規株式の売却が ETF 価格を押し下げ、二つは収束する。解約はディスカウントで取引される場合にループを逆回転させる。

現金設定とインカインド設定

米国固有の微妙だが重要な詳細がある。SEC はスポットビットコイン ETF の設定・解約を、インカインドではなく現金で行うよう上場時に求めた。現金設定では AP が米ドルを引き渡し、スポンサー(多くの場合カストディアンの執行デスクまたは指定トレーディングエージェントを通じて)がビットコインを購入する。インカインドでは AP が直接ビットコインを引き渡す。

現金設定は AP の規制上の立場を単純化する——AP 自身は暗号資産を保有・転送・接触する必要が一切ない——これがブローカー・ディーラーを参加させる上で鍵となった。トレードオフとして、現金受け取りからコイン取得までのインターバルにおける執行リスクをスポンサーが負い、そのスプレッドは若干のトラッキングエラーと取引コストの摩擦として株主に転嫁される。これは仮想的なインカインド構造と比較した場合のコストだ。一部商品をインカインド設定に移行する提案は既に流通しており、その仕組みは摩擦コストを削減するものとして注目する価値がある。

裁定が機能しなくなるとき

裁定は無条件には成立しない。AP が(a)スポット在庫を調達または放出でき、(b)設定から決済までのあいだポジションを資金調達でき、(c)ETF の取引時間中に発注をルーティングできること——これらすべてに依存している。それぞれに特定の失敗モードがある。

裏付けとなるスポット市場が急変した場合——週末の BTC 値動きが米国取引時間外に起きるのが典型例——月曜日の寄り付き時点で ETF はディスカバリーギャップを抱えることになる。AP は T+1 または T+2 の決済スケジュールでしか設定・解約できない一方、取引所価格はリアルタイムで動くため、そのギャップを即座に裁定することはできない。どのファンドでも小規模なプレミアム・ディスカウントの発生は観察されている。2020 年 3 月型の市場ストレスでは、固定利付 ETF が AP による裏付け在庫調達の困難から数日間にわたり表示 NAV の 5% 割れで取引された。スポット ETF 時代にそれに相当する大規模な事例はまだ観察されていないが、理論的な脆弱性は現実に存在する。

特定の AP が撤退した場合——信用上の理由、コンプライアンス上の理由、あるいは内部リスク枠の理由で——残りの AP が設定需要を吸収しなければならない。一年以上にわたって続いた Grayscale GBTC のディスカウントは完全な類似事例ではない(当時の GBTC はクローズドエンド型で解約メカニズムが存在しなかった)が、裁定チャネルが損なわれた際にラッパーの価格がいかに速く乖離するかを示している。

HYPE の上場がテンプレートについて示すこと

2025 年末に上場したスポット HYPE ETF は、ラッパーのテンプレートが新しい資産にどれほど迅速に拡張されるかを示す新鮮なデータポイントだ。初日取引ウィンドウで報告された早期出来高は~$900M に達し、報告が正確であれば、ETF 上場記録を塗り替えた 2024 年 1 月のスポット BTC 上場に照らしても遜色ない水準だ。

この数字の背後に二つの観察がある。

流通チャネルが重労働を担う

HYPE トークンそれ自体は、特定のデリバティブ特化型 L1 の ガバナンス とガスアセットだ。ETF 上場前の保有者ベースは、上場ラッパーを必要とする明確な理由を持たないオンチェーン参加者に集中していた。したがって初日の取引の大部分は構造的にいって新規マネーであり——裏付け資産を直接保有できない、または保有しようとしない投資家によるものだ。

これはビットコイン ETF が最初の 2 年間にわたって総体として示したことを確認するものだ。ラッパーは既存の保有者を主に転換するのではない。隣接するプール——RIA(登録投資顧問)、証券口座、退職金制度、SEC 登録証券を要件とする社内規程を持つ企業財務——に到達するのだ。ある資産が ETF に「値するかどうか」という問いは、より狭い問いに収束する。スポンサーの運営コストを正当化するだけの流通需要が存在するかどうか。

テンプレートはすでに標準化された

HYPE 商品は BTC・ETH ファンドとほぼ同一のアーキテクチャで上場した。現金設定、おなじみのスポンサー、おなじみの AP、そして少なくとも一部の発行体については Coinbase Custody をサブカストディアンとして。「新興資産」から「上場スポット ETF」までの道のりは、BTC のケースでは年単位を要したが、その後の資産については——使えるインデックスと必要な 19b-4 を提出する意思のある上場取引所さえあれば——数ヶ月に短縮されたように見える。

標準化は上場スピードに有利であり、構造的多様性には不利だ。米国市場に追加されるスポット暗号資産 ETF はすべて、同じカストディ集中、同じ現金設定の制約、同じ少数の AP を引き継ぐ。どれか単一の障害点——最大のカストディアン、最大の AP、参照取引所——へのシステミックなエクスポージャーは、商品が増えるたびに積み上がっていく。

ラッパーの中でビットコインが失うもの

Trezor 幹部の批判——ETF 形式はビットコインにとって最悪の結果だ——は、ハードウェアウォレット企業が自社利益のために語っているにすぎないと退けるのは簡単だ。だが、より丁寧に読み解く価値がある。その主張を修辞的な誇張を取り除いて整理すれば、ビットコインをコモディティ信託の持分証書と区別する特性こそが、ラッパーによって剥ぎ取られるものだということだ。それが重要かどうかは、なぜその資産を保有するのかに完全に依存する。

セルフカストディと検閲耐性

ETF の株主はビットコインを保有していない。ビットコインを保有する信託に対する請求権を保有しており、その請求権は指定された時間帯に規制取引所で取引可能な株式として表示される。カストディアンのコンプライアンスポリシー——制裁スクリーニング、取引モニタリング、地域制限——は、設計上の特徴として株主と裏付け資産のあいだに介在する。これは ETF の欠陥ではない。それゆえに ETF が承認可能だったのだ。

ビットコインを保有する理由がドル価格へのエクスポージャーであるなら、この違いは重要ではない。しかし、無記名証書の一方的管理から生じる特性——許可なくトランザクションを実行できること、単一の法的管轄の外で保有できること、特定の国家行為に対して検閲耐性を持つこと——そうした特性はラッパーを通じては残らない。ETF の株主はあらゆる実質的な意味において、国家が介在する保護と制約を全て含んだ専門信託のエクイティ保有者だ。

24 時間 365 日の決済が T+1・取引時間内に縮小される

ビットコインのベースレイヤーは週末も祝日も継続的にブロックを決済する。ETF の株式は DTCC を通じて T+1 で決済され、取引所の開場時間中にしか売買できない。日曜の朝にポジションを動かしたい保有者は、裏付け資産が何をしていようとそれができない。ラッパーはその定義的な特徴がその日程を打ち破ることにあった資産に、1970 年代の株式の決済カレンダーを押しつける。

大多数の投資家にとってこれは問題ではない。機関投資家のフローが通常、日曜の 流動性 を必要とすることはない。しかし 24 時間 365 日の決済に価値を見出していた特定の層——マーケットメーカー、国境を越えた送金業者、週末のオプション性を必要とするトレジャリー——にとって、ETF は直接保有の代替にならない。

ガバナンスとフォーク

ETF 株主はチェーンレベルの ガバナンス イベントに対して発言権を持たない。対立的なハードフォークが発生した場合、スポンサーが信託のどちら側を保有するかを決定し、フォーク後の資産を分配するか、売却するか、無視するかを判断する。2017 年の SegWit2x と Bitcoin Cash のエピソードは、機関投資家の BTC エクスポージャーの大多数がフォークポリシーを目論見書で規定した信託構造の中にあったとすれば、まったく異なる様相を呈していただろう。これは小規模資産においては仮定の話ではない。ラップされた資産の基盤チェーンで将来対立的な ガバナンス 上の決定が生じた場合、それは今や一定の部分がスポンサーとそのカストディアンに委任されているのだ。

手数料の侵食

ETF は経費率を課す。現行のスポット BTC ETF の手数料は、競争的な価格帯では年~0.15%〜0.25% 程度であり、古い商品や特殊な商品はより高い。長期保有の場合、これは一時的な取引・保管コストしか負担しないセルフカストディのポジションに対して、複利で相当な差を生む。その手数料はファンド運営コストを考えれば不合理ではない。ただし、直接保有者には存在しないコストであるという事実は変わらない。

得られるもの

以上はラッパーが付加するものを否定するためのものではない。監査可能性、標準化された税務申告、既存ポートフォリオインフラとの統合、ユーザー側のカストディエラーに対する保護(歴史的にビットコイン損失の最大の単一カテゴリー)、そして規制された資本プールにとっては、そもそもその資産を保有できること自体がある。エンダウメントや年金ファンドにとって、ETF は妥協ではない。コンプライアンス上の唯一の経路だ。Trezor の批判が言っているのは、これらのメリットが存在しないということではない。それらを純粋な付加価値として描くことが、反対側のトレードオフを見落とす、ということだ。

今後注視すべきこと

スポット暗号資産 ETF 市場の次のフェーズを形成するいくつかの構造的な問いがあり、それぞれ独自の観点から追い続ける価値がある。

カストディの分散化。 Coinbase Custody への集中が緩和されるかどうか——既存ファンドへのセカンダリーカストディアンの追加、または異なる体制で新商品が上場することによって——は、単一の最も重要な構造的リスク変数だ。支配的なカストディアンに影響する規制上または運営上のインシデントは、市場がまだ目にしていないストレステストとなる。

インカインド設定。 SEC がスポット暗号資産 ETF へのインカインド設定・解約への移行を認めた場合、トラッキングエラーは縮小し、ブローカー・ディーラーが裏付け資産に直接関与する意向を持つようになれば AP の数が増える可能性がある。これは純粋に機械的な変更だが、株主にとってのコストに実質的な影響をもたらす。

リハイポセケーションのドリフト。 ETF カストディ契約における現在の無貸し出しの立場は、設計上の選択であって規制上の床ではない。スポンサーが信託契約を改定して、ステーキング(PoS 資産の場合)、貸し出し、あるいはその他の遊休コインからの 利回り 生成を認める動きを注視すべきだ。そうした改定はそれぞれ、手数料比較だけでは捉えきれない形で株式のリスクプロファイルを変える。

AP 集中とストレス時の挙動。 スポット暗号資産 ETF の現行 AP セットは、最大手の固定利付・株式 ETF の AP セットと大きく重複している。本物の市場ストレスイベントが発生した際、これらのデスクの資本とリスク許容度は商品間で加算的ではない。次のマクロショック時のプレミアム・ディスカウントの挙動は、現在の平穏な市場でのトラッキングデータから見えるいかなるものより、ラッパーの頑健性についてより多くを語るだろう。

ガバナンスの委任。 より多くの資産がラップされるにつれて——特にアクティブなガバナンスを伴うプルーフ・オブ・ステーク資産——スポンサーがチェーンレベルの決定をどう処理するかという問いが実質的に重要になる。ETF スポンサーとそのカストディアンの少数グループの手に投票権またはステーキング権限が集中することは、オンチェーンコミュニティがまだ十分に消化していないガバナンスの集中だ。

ラッパーは暗号資産の救済でも最悪の結果でもない。特定のトレードオフを持つ特定の金融配管だ。正直な分析的立場とは、そのトレードオフを理解することであり、一括して受け入れることでも一括して拒絶することでもない。ETF が与えるもの——流通、コンプライアンス、統合——は本物だ。ETF が奪うもの——セルフカストディ、24 時間 365 日の決済、ガバナンス参加、検閲耐性——も本物だ。そのトレードが値するかどうかは、そもそもなぜその裏付け資産を欲していたのかという問いにまったく依存する。

引言

2025年底的两组数据,为本文试图解答的问题提供了背景框架。其一,现货HYPE ETF在美国正式上市,据报道首日成交量接近9亿美元,延续了现货BTC和ETH产品所确立的规律:每一只新上市的加密资产包装产品,都能在数小时内吸引机构资金涌入。其二,硬件钱包厂商Trezor的一位高管公开表示,ETF这种形式是比特币”最坏的结局”——它在提升可及性的同时,也掏空了这一资产之所以值得持有的核心属性。

这两种说法可以同时成立。ETF包装是加密行业有史以来最成功的分发机制,但它也从结构上根本改变了持有者实际拥有的东西。在一方的营销光环与另一方的意识形态排斥之间,存在一系列大多数报道都会略过的”管道问题”:币究竟由谁持有?份额如何与现货价格保持锚定?压力事件发生时会怎样?比特币最初的哪些属性能在包装之后得以保留?

本文将逐一梳理这些底层机制。我们将深入探讨连接发行人、授权参与者、托管方和做市商的四方架构;关键托管高度集中于美国单一机构的现象;维持资产净值(NAV)紧密跟踪的套利机制;以及每一位ETF份额持有者在隐性接受这一结构时所面临的法律、操作与理念层面的权衡取舍。HYPE的上市和Trezor的批评是本文的当代参照点,但这些结构性问题同样适用于当前已上市或待批准的任何现货加密ETF。

每一只现货加密ETF背后的四方结构

现货加密ETF常常被描述成一个被动容器:币进去,份额出来,价格跟踪。现实是,这背后是四个独立法律实体之间精密协调的运作,每个实体都有各自的利益驱动,也都有各自的失效节点。

发行人(Sponsor)

发行人——IBIT背后的贝莱德、FBTC背后的富达、Bitwise旗下的BITB产品等——是基金的发起方和推广方。发行人负责撰写招募说明书、设定管理费率、雇佣托管方,并从资产中抽取管理费。但发行人本身并不直接持有加密币,其角色更接近于总承包商,而非仓储方。

发行人的核心资产是分发关系:券商平台的接入、财务顾问的覆盖、指数的纳入,以及在全国性交易所上市的监管许可。这些分发渠道是自托管比特币所无法触达的,也是ETF存在的全部商业逻辑所在。

授权参与者(Authorized Participant,AP)

授权参与者(AP)是整个结构的机械核心。AP通常是大型经纪自营商——美国市场中包括Jane Street、Virtu、Cantor Fitzgerald、摩根大通证券部门及少数其他机构——它们与基金签有合约,享有直接申购和赎回份额的权利。

当终端投资者的需求推动ETF份额价格高于NAV时,AP向基金交付所需的申购篮子(在美国现行现货BTC ETF中为现金;某些司法管辖区则为实物币),并获得新发行的份额,再将其卖入市场。当份额折价时,AP反向操作。AP这样做并非出于义务,市场价格与NAV之间的价差就是它的套利利润。

任何一只基金的批准AP数量都很有限,且不同基金之间的AP高度重叠。同样那几家交易台,同时为IBIT、FBTC以及现在的HYPE产品做市。这并非偶然——成为AP的操作、信用和合规门槛相当高——但这也意味着做市风险的集中程度值得正视。

托管方(Custodian)

托管方持有实际的私钥。美国大多数现货比特币ETF的托管方是Coinbase Custody Trust Company,这是一家受纽约州特许设立的特殊目的信托公司。富达使用其自建的内部托管部门,少数规模较小的基金分散于BitGo、Anchorage或Gemini。但Coinbase在托管市场份额上的高度集中,在成熟金融产品类别中实属罕见,值得单独讨论,见下文。

托管方的职责范围明确:在申购时接收加密币,在赎回时释放加密币,其余资产存于冷钱包,并出具证明文件。根据现行ETF协议,托管方不得对加密币进行交易、对冲或出借——这一点与传统金融中的主经纪商安排有所不同。

做市商与交易所

做市商——往往与AP是同一家机构,只是身份不同——在上市交易所(通常为NYSE Arca、Cboe BZX或纳斯达克)持续提供双边报价。交易所本身提供撮合引擎、市场监察,以及使份额能够面向散户销售、并可纳入税收优惠账户的SEC注册场所。

终端投资者只与最后两层打交道:他们在交易所从做市商手中买入份额。其他一切——发行人与托管方的合约、AP的申购篮子、加密币流入冷钱包的过程——都在上游默默运行,对投资者不可见。

托管集中与Coinbase问题

美国现货比特币ETF群体中被引用最多的结构性特征是:绝大多数底层持币集中在同一家托管方——Coinbase Custody。多家主要发行人——包括贝莱德、灰度、Bitwise、Ark 21Shares、VanEck和Invesco Galaxy——在公开的10-K年报和招募说明书中,均将Coinbase列为初始托管方。富达是少数例外,使用其旗下的Fidelity Digital Asset Services。

这种集中状态有三个值得分别审视的后果:操作风险、市场结构风险,以及反身性出借风险。

操作风险

Coinbase Custody作为纽约州特许信托公司运营,受NYDFS监管,并以独立于Coinbase Inc.运营资产负债表的破产隔离结构持有资产。理论上,Coinbase Global的破产不应将ETF资产与债权人索赔相混同。但实际上,这一机制从未在当前托管规模下经过检验,有关加密资产破产隔离托管的法律文献仍然匮乏。发行人的招募说明书在风险因素章节中通常也承认这种不确定性。

操作层面——签名基础设施、人员、物理设施、HSM——同样高度单一。一旦Coinbase Custody发生严重操作事故,将同时波及美国绝大多数已上市现货BTC AUM。在传统金融中,几乎找不到一家次级托管方独自持有如此大比例的广泛营销资产类别的先例。

市场结构风险

Coinbase同时也是美国最大的合规现货交易所,并通过与上市交易所签订的市场监察信息共享协议,成为SEC最终认可现货比特币ETF申请时所援引的”具有重要规模的受监管市场”的参照市场。因此,同一家实体集多重角色于一身:(a) 托管方,(b) 通过指数提供商影响NAV计算的主要现货交易场所,以及 (c) 其股票本身也是上市证券的上市公司。

这些角色本身并不构成利益冲突,且每项均在独立的法律实体中隔离。但将托管、价格发现和市场监察集中于同一企业集团,是一种在大多数其他上市市场中都不会被容忍的结构性特征。

出借与再抵押

据我们所知,在现行ETF协议下,托管方不得出借所持加密币。这使该包装结构有别于主经纪商安排,也有别于2022年因涉及再抵押而相继崩溃的无监管加密借贷机构。若未来某发行人修改其信托协议以允许对闲置币产生收益——这是显而易见的商业诱惑——份额的风险状况将发生实质性变化。任何招募说明书的读者都应直接核查托管和出借相关章节,而不能想当然地认为当前的不出借立场将永久维持。

申购、赎回与维持价格准确的套利机制

ETF份额能够紧密跟踪NAV——美国最大现货BTC产品历史上通常在几个基点以内——原因并非基金承诺了某种盯住关系,而是一小群专业套利者依据合约能够从任何偏差中获利。

机械运作循环

以简化的申购周期为例。假设一份ETF份额对应0.0001 BTC。若该ETF在交易所的交易价格隐含的每份价值为0.00011 BTC,而现货比特币参考价格较低,则AP可以:

- 按参考价格在Coinbase或跨多个场所买入现货比特币。

- 将该比特币或等值现金(取决于基金的申购模式)连同相应费用交付给发行人。

- 获得一批新发行的ETF份额——通常以1万份以上为一个申购单位。

- 将这批份额以较高价格卖入市场。

AP赚取价差,扣除交易成本和融资费用后即为净利润。买入现货的行为推动参考价格上行;卖出新发行份额的行为压低ETF价格;两者趋于收敛。折价时,赎回操作则沿相反方向运行。

现金申购与实物申购

一个微妙但影响深远的美国特有细节:SEC要求现货比特币ETF在上市之初采用现金申购与赎回,而非实物申购。在现金申购模式下,AP交付美元,发行人(通过代理,通常是托管方的执行台或指定交易代理)再买入比特币。若采用实物申购,AP将直接交付比特币。

现金申购简化了AP的监管处境——AP本身无需持有、转移或接触加密币——这是让经纪自营商接受这一结构的关键。代价是,发行人在接受现金与完成购币之间承担执行风险,该价差以略高的跟踪误差和略高的交易成本拖累的形式转嫁给份额持有者,相比假设中的实物申购结构摩擦成本更高。将部分产品切换为实物申购的提案已在业界流传;这一机制值得持续关注,因为它能消除一项摩擦成本来源。

套利失效时会发生什么

套利机制并非无条件成立。它依赖于AP能够 (a) 获取或抛售现货库存,(b) 在申购结算期间为头寸融资,以及 (c) 在ETF交易时段内完成路由下单。这三点各有其特定的失效场景。

若底层现货市场出现跳空——美国交易时段以外的周末BTC大幅波动是典型案例——ETF周一开盘时将面临一个价格发现缺口,AP无法立即通过套利消除,因为他们只能在T+1或T+2的结算周期内完成申购或赎回,而交易所价格实时波动。每一只基金都曾观察到小幅溢价/折价偏离。2020年3月市场压力期间,固定收益ETF相对于公告NAV折价高达5%,持续数日,原因是AP无法按参考价格获取底层资产;在现货ETF时代,类似规模的加密市场压力事件尚未出现,但理论上的脆弱性是真实存在的。

若某一AP因信用原因、合规原因或内部风险限额原因暂停运作,其余AP必须承接申购需求。灰度GBTC在转型为ETF之前折价持续超过一年,并非完全相同的案例(彼时GBTC是封闭式结构,完全没有赎回机制),但它生动展示了当套利渠道受阻时,包装产品的价格能以多快的速度脱轨。

HYPE上市揭示的模板化趋势

2025年底上市的现货HYPE ETF,为这套包装模板向新兴资产快速延伸提供了最新佐证。据报道,初始交易窗口内的早期成交量接近9亿美元,这一数字即便以2024年1月现货BTC上市的标准衡量也相当强劲——而那次本身就打破了ETF上市记录。

这一数字背后有两点值得关注。

分发渠道才是关键驱动力

HYPE代币本身是一条专注于衍生品的Layer 1的治理和Gas资产。ETF上市前,其持有者高度集中于链上参与者,这些人对上市包装产品并无明显需求。因此,上市首日的成交量在很大程度上是结构性地来自增量资金——那些无法或不愿直接持有底层资产的投资者。

这印证了比特币ETF在头两年所集体验证的规律:包装产品并不主要转化现有持有者,而是触达相邻的新资金池——注册投资顾问(RIA)、券商账户、退休工具、政策要求只能持有SEC注册证券的企业金库。一项资产是否”值得”拥有ETF,最终归结为一个更狭窄的问题:分发层面的需求是否足以覆盖发行人的运营成本。

模板已高度标准化

HYPE产品的上市采用了与BTC和ETH基金大致相同的架构:现金申购、熟悉的发行人、熟悉的AP,以及至少部分发行人将Coinbase Custody作为次级托管方。从”新兴资产”到”上市现货ETF”的路径,已从比特币所经历的数年压缩至后续资产的数月——前提是有可用的指数和愿意提交19b-4文件的上市交易所。

标准化有利于加快上市速度,却不利于结构多样性。美国市场每新增一只现货加密ETF,都继承了同样的托管集中、同样的现金申购限制和同样的少数几家AP。对任何单一失效节点的系统性敞口——最大托管方、最大AP、参考交易所——随着每一只新产品的加入而不断累积。

比特币在包装后失去了什么

Trezor高管的批评——ETF形式是比特币最坏的结局——很容易被斥为硬件钱包厂商在为自身利益代言。但这一论点值得更认真地对待。其核心论点去掉修辞外壳后是:正是那些让比特币区别于任何大宗商品信托不记名份额的属性,恰恰是包装所剥夺的属性。这是否重要,完全取决于持有这一资产的初衷。

自托管与抗审查

ETF份额持有者持有的不是比特币,而是对一个持有比特币的信托的索取权,且该索取权以可在注册交易所指定时段交易的份额形式存在。托管方的合规政策——制裁筛查、交易监控、司法管辖限制——被设计性地介于份额持有者与底层资产之间。这不是ETF的缺陷,而是它得以获批的原因。

如果持有比特币的目的是获得其美元价格敞口,这一区别无关紧要。但如果目的在于不记名工具单边控制所带来的任何属性——无需许可即可交易的能力、在任何单一法律管辖区之外持有的能力、抵御特定国家行动的抗审查能力——这些属性都无法在包装中存续。ETF份额持有者在一切实质意义上都是一个特殊信托的权益持有者,并承担着由此带来的一切国家中介式的保护与约束。

7×24结算压缩为T+1加交易时段限制

比特币基础层持续出块结算,包括周末和节假日。ETF份额通过DTCC进行T+1结算,且只在交易所交易时段内可交易。一位希望在周日上午调整仓位的持有者无能为力,无论底层资产正在发生什么。这一包装将1970年代股票的结算日历强加于一项以打破该日历为核心特征的资产之上。

对大多数投资者而言,这无关紧要;机构资金流动通常不在乎周日流动性。但对于那些特别看重7×24结算的特定持有者群体——做市商、跨境汇款方、需要周末操作灵活性的金库——ETF无法替代直接持有。

治理与分叉

ETF份额持有者在链级治理事件中没有任何发言权。若发生争议性硬分叉,发行人将决定信托持有分叉的哪一方,以及是否分配、出售或无视分叉资产。如果2017年SegWit2x和比特币现金事件发生时,大多数机构BTC敞口已坐落于有招募说明书定义分叉政策的信托结构中,结局将大相径庭。对于市值较小的资产,这并非假设:被包装资产底层链上任何未来的争议性治理决定,现在都将部分委托给发行人及其托管方代为处置。

费用拖累

ETF收取管理费。当前现货BTC ETF的费率,价格竞争层约在0.15%至0.25%之间,较早期或专项产品收费更高。长期持有下,这一费用相较于只需承担一次性交易和托管成本的自托管仓位,复利效应相当可观。该费用考虑到基金运营成本并不过分,但对于直接持有者而言,这是一项实实在在并不存在的成本。

包装带来了什么

以上所述并非否认包装结构的价值。可审计性、标准化税务报告、与现有投资组合基础设施的集成、对用户端托管失误的防护(这是历史上比特币损失最大的单一类别),以及——对于受监管的资金池而言——能够持有该资产本身。对于捐赠基金或养老金而言,ETF并非一种妥协,而是合规持仓的唯一可行路径。Trezor的批评并非认为这些好处不存在,而是认为将其框架为纯粹的增量价值,遮蔽了账本另一侧的权衡取舍。

未来值得关注的方向

几个结构性问题将塑造现货加密ETF市场的下一阶段,每一个都值得单独追踪。

托管多元化。 Coinbase Custody的集中度能否分散——无论是通过现有基金引入次级托管方,还是新产品以不同安排上市——是目前最重要的单一结构性风险变量。任何影响主导托管方的监管或操作事故,都将是市场迄今从未经历的压力测试。

实物申购。 若SEC允许现货加密ETF切换至实物申购与赎回,跟踪误差有望收窄,随着经纪自营商愿意直接接触底层资产,AP群体也可能扩大。这是一项纯粹的机制性变化,但对份额持有者有着实质性的成本影响。

再抵押漂移。 ETF托管协议中当前的不出借立场是一种设计选择,而非监管底线。应密切关注发行人是否修改信托协议,以允许对闲置币进行质押(针对PoS资产)、出借或其他收益生成操作。每一次此类修改都将以单纯的费率比较所无法捕捉的方式,实质性地改变份额的风险状况。

AP集中度与压力行为。 当前现货加密ETF的AP群体与最大规模固定收益和权益ETF的AP群体高度重叠。在真正的市场压力事件中,这些交易台的资本和风险承担能力并不会因产品线增加而叠加。下一次宏观冲击期间溢价和折价的表现,将比目前平静市场下的任何跟踪数据,更能说明这一包装结构的稳健性。

治理委托。 随着越来越多的资产被包装——尤其是具有活跃治理的权益证明(PoS)资产——发行人如何处理链级决策的问题变得至关重要。投票权或质押权高度集中于少数ETF发行人及其托管方,是链上社区尚未充分消化的一种治理集中现象。

包装结构既非加密行业的救星,也非其最坏的结局。它是一段具有特定权衡取舍的金融管道,诚实的分析立场是理解这些取舍,而非不加分辨地全盘接受或拒绝。ETF所给予的——分发、合规、集成——是真实的。它所带走的——自托管、7×24结算、治理参与、抗审查——同样是真实的。这笔交易是否值得做,完全取决于你最初持有底层资产的原因。

Introducción

Dos datos de finales de 2025 enmarcan la pregunta que este artículo intenta responder. Primero, los ETFs de HYPE al contado debutaron en Estados Unidos con un volumen reportado en el primer día cercano a los $900M, extendiendo el patrón establecido por los productos de BTC y ETH al contado: cada nuevo wrapper cripto listado atrae flujo institucional en cuestión de horas. Segundo, un alto ejecutivo del fabricante de carteras de hardware Trezor argumentó públicamente que el formato ETF es el “peor resultado posible” para bitcoin — una victoria en términos de accesibilidad que vacía las propiedades que hacían al activo digno de ser accedido.

Ambas afirmaciones pueden ser ciertas. El wrapper ETF es el mecanismo de distribución más exitoso que el ecosistema cripto ha logrado construir; y al mismo tiempo es una transformación estructural de lo que los tenedores realmente poseen. Entre el barniz de marketing de un lado y el rechazo ideológico del otro, existe un conjunto de preguntas sobre la fontanería interna que la mayoría de los análisis esquiva: quién custodia realmente las monedas, cómo se mantienen las participaciones ligadas al precio al contado, qué ocurre durante un evento de estrés, y cuáles de las propiedades originales de bitcoin sobreviven al empaquetado.

Este artículo recorre esa fontanería. Analizamos la arquitectura de cuatro actores que conecta al sponsor, el participante autorizado, el custodio y el creador de mercado; la concentración del custodio clave en un único venue estadounidense; el mecanismo de arbitraje que mantiene el valor liquidativo ajustado; y los compromisos — legales, operativos y filosóficos — que cualquier tenedor de participaciones de ETF acepta implícitamente. El lanzamiento de HYPE y la crítica de Trezor sirven como anclas contemporáneas, pero las preguntas estructurales aplican por igual a cualquier ETF de cripto al contado que cotice hoy o aguarde aprobación.

Los cuatro actores dentro de todo ETF de cripto al contado

Un ETF de cripto al contado se describe a menudo como si fuera un contenedor pasivo: entran monedas, salen participaciones, el precio sigue al subyacente. La realidad es una danza coordinada entre cuatro entidades jurídicas diferenciadas, cada una con sus propios incentivos y sus propios puntos de fallo.

El sponsor

El sponsor — BlackRock en el caso de IBIT, Fidelity para FBTC, Bitwise para su producto BITB, y así sucesivamente — es el emisor y el promotor del fondo. El sponsor redacta el prospecto, fija el ratio de gastos, contrata al custodio y cobra las comisiones de gestión sobre el total de activos. Sin embargo, el sponsor no custodia las monedas directamente. Se parece más a un contratista general que a un almacenista.

El activo central del sponsor es su red de distribución: integraciones con plataformas de corretaje, cobertura de asesores financieros, inclusión en índices y el aval regulatorio para cotizar en una bolsa nacional. Esos canales de distribución son lo que un bitcoin en autocustodia no puede alcanzar, y son la razón comercial de la existencia de los ETFs.

El participante autorizado

El participante autorizado (AP, por sus siglas en inglés) es el corazón mecánico de la estructura. Los APs son típicamente grandes broker-dealers — Jane Street, Virtu, Cantor Fitzgerald, el brazo de valores de JPMorgan, y un puñado más en el mercado estadounidense — que poseen derechos contractuales para crear y redimir participaciones directamente con el fondo.

Cuando la demanda de los inversores finales empuja las participaciones del ETF a una prima sobre el NAV, el AP entrega la cesta requerida (en los ETFs de BTC al contado vigentes en EE. UU., en efectivo; en algunas jurisdicciones, en monedas) al fondo y recibe participaciones recién emitidas que vende al mercado. Cuando las participaciones cotizan con descuento, el AP ejecuta el proceso inverso. El AP no hace esto como un favor; el diferencial entre el precio de mercado y el NAV es su margen de arbitraje.

Solo un número reducido de firmas está aprobado como AP para un fondo determinado, y la superposición entre fondos es significativa. Los mismos escritorios están haciendo mercado en IBIT, FBTC y ahora en los productos de HYPE. Esto no es accidental — los requisitos operativos, crediticios y de cumplimiento para ser AP son exigentes — pero concentra el riesgo de creación de mercado de formas que vale la pena nombrar.

El custodio

El custodio custodia las claves privadas reales. Para la mayoría de los ETFs de bitcoin al contado en EE. UU., ese custodio es Coinbase Custody Trust Company, una sociedad fiduciaria de propósito limitado registrada en Nueva York. Fidelity utiliza su propio brazo de custodia interno, y algunos fondos más pequeños se distribuyen entre BitGo, Anchorage o Gemini. Pero la concentración de cuota de mercado en Coinbase es inusual para una categoría de producto financiero maduro y merece su propia sección más adelante.

La función del custodio está acotada: recibir monedas cuando se producen creaciones, liberarlas cuando se producen redenciones, mantener el resto en almacenamiento en frío y emitir atestaciones. El custodio no opera, no cubre ni presta las monedas bajo los acuerdos estándar de ETF — una distinción importante respecto a los acuerdos de prime brokerage en las finanzas tradicionales.

El creador de mercado y la bolsa

El creador de mercado — a menudo la misma firma que el AP, con un sombrero distinto — proporciona cotizaciones continuas a doble cara en la bolsa listada (típicamente NYSE Arca, Cboe BZX o Nasdaq). La bolsa en sí proporciona el motor de emparejamiento de órdenes, la vigilancia del mercado y el venue registrado ante la SEC que permite vender las participaciones al inversor minorista y mantenerlas en cuentas con ventajas fiscales.

El inversor final interactúa únicamente con las dos últimas capas: compra una participación en una bolsa a un creador de mercado. Todo lo demás — el contrato del sponsor con el custodio, la cesta de creación del AP, el movimiento de monedas al almacenamiento en frío — ocurre de forma invisible en el tramo anterior.

La concentración en custodia y el problema de Coinbase

La característica estructural más citada del conjunto de ETFs de bitcoin al contado en EE. UU. es que una gran mayoría de las monedas subyacentes se encuentran en manos de un único custodio: Coinbase Custody. Las divulgaciones públicas en los 10-K y prospectos de la mayoría de los grandes sponsors — incluidos BlackRock, Grayscale, Bitwise, Ark 21Shares, VanEck e Invesco Galaxy — designan a Coinbase como custodio en el lanzamiento. Fidelity es la excepción notable entre los grandes actores, al utilizar Fidelity Digital Asset Services.

Esta concentración tiene tres consecuencias que vale la pena examinar por separado: riesgo operativo, riesgo de estructura de mercado y riesgo de préstamo reflexivo.

Riesgo operativo

Coinbase Custody opera como una sociedad fiduciaria autorizada por el Estado de Nueva York, sujeta a la supervisión del NYDFS, y mantiene los activos en estructuras aisladas de quiebra separadas del balance operativo de Coinbase Inc. En principio, una quiebra de Coinbase Global no debería mezclar los activos del ETF con las reclamaciones de los acreedores. En la práctica, esto nunca ha sido probado a la escala del libro de custodia actual, y la literatura jurídica sobre custodia cripto aislada de quiebra sigue siendo escasa. Los prospectos de los sponsors generalmente reconocen esta incertidumbre en sus factores de riesgo.

La superficie operativa — infraestructura de firma, personal, instalaciones físicas, HSMs — también es singular. Un incidente operativo grave en Coinbase Custody afectaría simultáneamente a la mayoría del AUM de los ETFs de BTC al contado listados en EE. UU. No existe un análogo evidente en las finanzas tradicionales donde un único subcustodio concentre esta participación de una clase de activo ampliamente comercializada.

Riesgo de estructura de mercado

Coinbase es también el mayor exchange regulado al contado de EE. UU. y, a través de su acuerdo de intercambio de información de vigilancia con las bolsas listadas, es el mercado de referencia que proporcionó el argumento del “mercado regulado de tamaño significativo” que la SEC finalmente aceptó para la aprobación del bitcoin al contado. La misma entidad es, por tanto: (a) el custodio, (b) un venue de contado importante cuyo precio influye en los cálculos del NAV a través de los proveedores de índices, y (c) una empresa pública cuya renta variable es en sí misma un instrumento listado.

Ninguno de estos roles es per se conflictivo, y cada uno está separado en entidades jurídicas distintas. Sin embargo, la consolidación de custodia, descubrimiento de precios y vigilancia en una sola familia corporativa es una característica estructural que no sería tolerada en la mayoría de los demás mercados listados.

Préstamo y rehipotecación

Bajo los acuerdos de ETF actuales de los que tenemos conocimiento, el custodio no presta las monedas. Esto diferencia el wrapper de los acuerdos de prime brokerage o de los prestamistas cripto no regulados cuyos fracasos en 2022 sí involucraron rehipotecación. Si en el futuro un sponsor modifica su acuerdo de fideicomiso para permitir la generación de rendimiento sobre las monedas inactivas — una tentación comercial evidente — el perfil de riesgo de las participaciones cambia de forma material. Los lectores de cualquier prospecto deberían verificar directamente las secciones de custodia y préstamo, en lugar de asumir que la postura actual de no préstamo es permanente.

Creación, redención y el arbitraje que mantiene el precio honesto

La razón por la que las participaciones de un ETF siguen al NAV de cerca — históricamente dentro de unos pocos puntos básicos para los mayores productos de BTC al contado en EE. UU. — no es que el fondo garantice un anclaje. Es que un pequeño grupo de arbitrajistas profesionales está posicionado contractualmente para beneficiarse de cualquier desviación.

El ciclo mecánico

Consideremos un ciclo de creación simplificado. Supongamos que una participación del ETF representa 0.0001 BTC. Si el ETF cotiza en la bolsa a un precio que implica 0.00011 BTC por participación mientras el bitcoin al contado se encuentra en el nivel de referencia inferior, un AP puede:

- Comprar bitcoin al contado al precio de referencia, ya sea en Coinbase o en una cesta de venues.

- Entregar ese bitcoin o una cantidad equivalente en efectivo (dependiendo del modelo de creación del fondo) al sponsor, junto con cualquier comisión aplicable.

- Recibir un bloque de participaciones del ETF recién emitidas — típicamente en unidades de creación de 10.000 o más participaciones.

- Vender esas participaciones al mercado al precio elevado.

El AP se embolsa el diferencial, menos los costes de transacción y financiación. El acto de comprar al contado empuja el precio de referencia al alza; el acto de vender nuevas participaciones empuja el precio del ETF a la baja; los dos convergen. Las redenciones ejecutan el ciclo en sentido inverso cuando las participaciones cotizan con descuento.

Creaciones en efectivo versus creaciones en especie

Un detalle sutil pero de gran consecuencia específico de EE. UU.: la SEC exigió que los ETFs de bitcoin al contado utilizaran creaciones y redenciones en efectivo en lugar de en especie en el momento del lanzamiento. Bajo las creaciones en efectivo, el AP entrega dólares y el sponsor (a través de un agente, a menudo el escritorio de ejecución del custodio o un agente de negociación designado) compra el bitcoin. En la modalidad en especie, el AP entregaría bitcoin directamente.

Las creaciones en efectivo simplifican la posición regulatoria del AP — el AP en sí nunca tiene que mantener, transferir ni tocar cripto — lo que fue fundamental para que los broker-dealers se sintieran cómodos. La contrapartida es que el sponsor asume el riesgo de ejecución en el intervalo entre aceptar el efectivo y adquirir las monedas, y ese diferencial se traslada a los accionistas en forma de un error de seguimiento ligeramente mayor y un mayor arrastre por coste de transacción respecto a una estructura hipotética en especie. Han circulado propuestas para migrar algunos productos a creaciones en especie; la mecánica merece seguimiento porque reduciría una fuente de coste friccional.

Qué ocurre cuando el arbitraje falla

El arbitraje no es incondicional. Depende de que los APs puedan (a) obtener o descargar inventario al contado, (b) financiar la posición entre la creación y la liquidación, y (c) enrutar órdenes durante el horario de negociación del ETF. Cada uno de estos factores puede fallar de formas específicas.

Si el mercado subyacente al contado sufre un gap — el movimiento de BTC en fin de semana fuera del horario de negociación estadounidense es el caso canónico — el ETF abre el lunes con una brecha de descubrimiento de precio que el AP no puede eliminar de inmediato mediante arbitraje, porque solo puede crear o redimir con un calendario de liquidación T+1 o T+2 mientras el precio en la bolsa se mueve en tiempo real. Se han observado pequeñas excursiones de prima y descuento en todos los fondos. Durante el estrés de mercado al estilo de marzo de 2020 en los mercados tradicionales, los ETFs de renta fija cotizaron con descuentos del 5% sobre el NAV declarado durante días porque los APs no podían obtener el inventario subyacente al precio de referencia; un equivalente cripto a gran escala aún no se ha observado en la era de los ETFs al contado, pero la fragilidad teórica es real.

Si un AP específico se retira — por razones crediticias, de cumplimiento o de límites de riesgo internos — los APs restantes deben absorber la demanda de creación. El descuento de Grayscale GBTC que persistió durante más de un año antes de su conversión a ETF no es un análogo exacto (GBTC era de tipo cerrado en ese momento, sin ningún mecanismo de redención), pero ilustra con qué rapidez el precio del wrapper puede desacoplarse cuando el canal de arbitraje está deteriorado.

Lo que el lanzamiento de HYPE revela sobre el modelo

Los ETFs de HYPE al contado que se lanzaron a finales de 2025 ofrecen un nuevo punto de datos sobre la rapidez con que la plantilla del wrapper se extiende ahora a activos más recientes. El volumen inicial reportado se acercó a los $900M en la ventana de negociación inicial, una cifra que, si los reportes son exactos, sería sólida incluso comparada con los lanzamientos de BTC al contado de enero de 2024 — que a su vez batieron récords de lanzamiento de ETFs.

Bajo este número descansan dos observaciones.

El canal de distribución hace el trabajo pesado

El token HYPE en sí es un activo de gobernanza y gas para un L1 específico orientado a derivados. Su base de tenedores pre-ETF estaba concentrada en participantes on-chain que no tenían una necesidad evidente de un wrapper listado. El volumen en los primeros días de negociación fue, por construcción en gran medida, dinero nuevo — inversores que no podían o no querían mantener el subyacente directamente.

Esto confirma lo que los ETFs de bitcoin demostraron en conjunto durante sus primeros dos años: el wrapper no convierte principalmente a los tenedores existentes. Alcanza un pool adyacente — RIAs, cuentas de corretaje, vehículos de jubilación, tesorerías corporativas con mandatos que exigen valores registrados ante la SEC. La pregunta de si un activo determinado “merece” un ETF se reduce a una pregunta más concreta: ¿hay suficiente apetito de distribución para justificar el coste operativo del sponsor?

La plantilla ya está estandarizada

Los productos de HYPE se lanzaron con prácticamente la misma arquitectura que los fondos de BTC y ETH: creaciones en efectivo, sponsors conocidos, APs conocidos y — para al menos algunos emisores — Coinbase Custody como subcustodio. El camino desde “activo novedoso” hasta “ETF al contado listado” se ha comprimido de años (en el caso de BTC) a lo que parece ser meses para los activos subsiguientes, asumiendo un índice funcional y una bolsa listada dispuesta a presentar el 19b-4 requerido.

La estandarización es favorable para la velocidad de lanzamiento y perjudicial para la diversidad estructural. Cada ETF de cripto al contado incremental añadido al mercado estadounidense hereda la misma concentración de custodia, la misma limitación de creación en efectivo y el mismo puñado de APs. La exposición sistémica a cualquier punto único de fallo — el custodio dominante, el AP más grande, el exchange de referencia — crece con cada producto nuevo.

Lo que bitcoin pierde dentro del wrapper

La crítica del ejecutivo de Trezor — que el formato ETF es el peor resultado para bitcoin — es fácil de desestimar como el discurso de quien defiende su negocio de carteras de hardware. Merece una lectura más cuidadosa. El argumento, despojado de la retórica, es que las propiedades que distinguen a bitcoin de una participación al portador en cualquier fideicomiso de materias primas son precisamente las propiedades que el wrapper elimina. Si eso importa depende de por qué uno mantiene el activo.

Autocustodia y resistencia a la censura

El accionista de un ETF no posee bitcoin. Posee un derecho sobre un fideicomiso que mantiene bitcoin, y ese derecho se denomina en una participación negociable en una bolsa registrada durante horarios específicos. Las políticas de cumplimiento del custodio — filtrado de sanciones, monitoreo de transacciones, restricciones jurisdiccionales — se interponen entre el accionista y el activo subyacente por diseño. Esto no es un defecto del ETF; es la razón por la que el ETF pudo ser aprobado.

Si el motivo para mantener bitcoin es la exposición a su precio en dólares, esta distinción es irrelevante. Si el motivo es cualquiera de las propiedades que se derivan del control unilateral de un instrumento al portador — la capacidad de transaccionar sin permiso, de mantener el activo fuera de cualquier jurisdicción legal única, de ser resistente a la censura frente a una acción estatal específica — esas propiedades no sobreviven al wrapper. El accionista del ETF es, en todos los sentidos significativos, un tenedor de capital en un fideicomiso especializado, con todas las protecciones y restricciones mediadas por el Estado que ello conlleva.

La liquidación continua se reduce a T+1 con horario de negociación

La capa base de bitcoin liquida bloques de forma continua, fines de semana y días festivos incluidos. Las participaciones del ETF liquidan T+1 a través de la DTCC y solo se negocian durante el horario de la bolsa. Un tenedor que quiera reposicionarse un domingo por la mañana no puede hacerlo, independientemente de lo que esté haciendo el subyacente. El wrapper impone el calendario de liquidación de la renta variable de los años setenta a un activo cuya característica definitoria era romper ese calendario.

Para la mayoría de los inversores, esto no es un problema; el flujo institucional generalmente no requiere liquidez los domingos. Para el subconjunto específico de tenedores que valoraban la liquidación continua — creadores de mercado, remesadores transfronterizos, tesorerías que necesitaban opcionalidad de fin de semana — el ETF no es un sustituto de la propiedad directa.

Gobernanza y forks

Un accionista del ETF no tiene voz en los eventos de gobernanza a nivel de cadena. Si se produce un hard fork controvertido, el sponsor decide qué lado del fork mantiene el fideicomiso y si distribuir, vender o ignorar el activo bifurcado. Los episodios de SegWit2x y Bitcoin Cash de 2017 habrían tenido un aspecto muy distinto si la mayoría de la exposición institucional a BTC hubiera estado dentro de estructuras fiduciarias con políticas de fork definidas en el prospecto. Esto no es hipotético para activos de menor capitalización: cualquier decisión de gobernanza controvertida futura en la cadena subyacente de un activo empaquetado queda ahora parcialmente delegada a los sponsors y sus custodios.

Arrastre por comisiones

Los ETFs cobran ratios de gastos. Las comisiones actuales de los ETFs de BTC al contado oscilan entre aproximadamente el 0,15% y el 0,25% en el segmento más competitivo en precio, con productos más antiguos o especializados cobrando más. A lo largo de un período de tenencia prolongado, esto se acumula de forma significativa respecto a una posición en autocustodia que solo paga costes únicos de transacción y custodia. La comisión no es irrazonable dado el coste operativo de gestionar el fondo; simplemente es un coste real que no existe para los tenedores directos.

Lo que se gana

Nada de lo anterior pretende desestimar lo que el wrapper aporta. Auditabilidad, informes fiscales estandarizados, integración con la infraestructura de cartera existente, protección frente a errores de custodia por parte del usuario (la mayor categoría individual de pérdidas históricas de bitcoin) y — para los pools de capital regulados — la posibilidad de mantener el activo en absoluto. Para un endowment o un fondo de pensiones, el ETF no es un compromiso; es el único camino de cumplimiento hacia la exposición. La crítica de Trezor no es que estos beneficios no existan. Es que presentarlos como puramente aditivos ignora la contrapartida que figura en el otro lado del balance.

Qué observar de aquí en adelante

Varias preguntas estructurales darán forma a la próxima fase del mercado de ETFs de cripto al contado, y cada una merece seguimiento por sus propios méritos.

Diversificación de la custodia. Si la concentración en Coinbase Custody se deshace — mediante la incorporación de custodios secundarios a los fondos existentes, o a través de nuevos productos que se lancen con acuerdos distintos — es la variable de riesgo estructural más importante a monitorear. Cualquier incidente regulatorio u operativo que afecte al custodio dominante será una prueba de estrés que el mercado aún no ha vivido.

Creación en especie. Si la SEC permite el cambio a creaciones y redenciones en especie para los ETFs de cripto al contado, el error de seguimiento debería reducirse y el conjunto de APs podría ampliarse a medida que los broker-dealers se muestren dispuestos a tocar el subyacente directamente. Se trata de un cambio puramente mecánico con implicaciones reales de coste para los accionistas.

Deriva hacia la rehipotecación. La postura actual de no préstamo en los acuerdos de custodia de ETFs es una decisión de diseño, no un límite regulatorio. Hay que estar atentos a si los sponsors modifican los acuerdos de fideicomiso para permitir el staking (en el caso de activos PoS), préstamos u otra generación de rendimiento sobre monedas inactivas. Cada enmienda de este tipo cambia el perfil de riesgo de las participaciones de formas que las comparaciones de comisiones por sí solas no capturan.

Concentración de APs y comportamiento bajo estrés. El conjunto actual de APs para los ETFs de cripto al contado se superpone en gran medida con el de los mayores ETFs de renta fija y renta variable. En un evento de estrés de mercado genuino, el capital y el apetito de riesgo en estos escritorios no es aditivo entre líneas de productos. El comportamiento de las primas y descuentos durante el próximo shock macroeconómico será más informativo sobre la robustez del wrapper que cualquier dato de seguimiento visible en las actuales condiciones de mercado tranquilo.

Delegación de gobernanza. A medida que se empaquetan más activos — en particular activos proof-of-stake con gobernanza activa — la cuestión de cómo gestionan los sponsors las decisiones a nivel de cadena se vuelve material. Una concentración de autoridad de voto o staking en manos de un pequeño conjunto de sponsors de ETFs y sus custodios es una concentración de gobernanza que las comunidades on-chain no han absorbido del todo.

El wrapper no es ni la salvación del ecosistema cripto ni su peor resultado. Es un trozo específico de fontanería financiera con compromisos específicos, y la postura analítica honesta es comprender esos compromisos en lugar de adoptarlos o rechazarlos en bloque. Lo que el ETF ofrece — distribución, cumplimiento, integración — es real. Lo que elimina — autocustodia, liquidación continua, participación en la gobernanza, resistencia a la censura — también es real. Si el intercambio vale la pena depende enteramente de por qué uno quería el activo subyacente en primer lugar.

Read next다음으로 읽기次に読む继续阅读Leer a continuación

The Quantum Threat to Bitcoin's Exposed Coins

A technical analysis of how quantum computing endangers reused Bitcoin addresses, which UTXOs are exposed, and what post-quantum migration would require.

[BTCFi Series 6] Babylon vs EigenLayer Compared

A structural comparison of Babylon's Bitcoin-native staking and EigenLayer's ETH restaking — slashing, rewards, operator selection, and downstream effects.

[BTCFi Series 5] Babylon and the BTCFi Security-Extension Ecosystem: An In-Depth Analysis of the Financialization of Bitcoin Security

An in-depth analysis of Babylon and its expanding ecosystem that seeks to transform Bitcoin from a mere store of value into "productive capital" for the Web3 ecosystem.

Follow the next market structure breakdown 다음 시장 구조 분석 받기 次の市場構造分析をフォロー 关注下一篇市场结构分析 Sigue el próximo análisis de estructura de mercado

New Steadyrain research is published several times a week across DeFi risk, BTCFi, stablecoins, and RWA. Steadyrain은 DeFi 리스크, BTCFi, 스테이블코인, RWA 분석을 매주 여러 차례 발행합니다. SteadyrainはDeFiリスク、BTCFi、ステーブルコイン、RWAの分析を毎週公開しています。 Steadyrain 每周发布 DeFi 风险、BTCFi、稳定币和 RWA 研究。 Steadyrain publica análisis sobre riesgo DeFi, BTCFi, stablecoins y RWA varias veces por semana.